Advertisement

- Canada

- /

- Aerospace & Defense

- /

- TSX:MDA

MDA Space (TSX:MDA) Valuation Check as RADARSAT+ Contracts and Debt Refinance Reshape Growth Outlook

Simply Wall St

Reviewed by Simply Wall St

MDA Space (TSX:MDA) just lined up two important pillars for its next chapter: fresh government work around RADARSAT and a C$250 million debt refinancing that reshapes its balance sheet for growth.

See our latest analysis for MDA Space.

The RADARSAT wins and debt reshuffle land as the stock recalibrates, with a 7 day share price return of 7.1% but a 1 year total shareholder return of minus 14.5%, following a powerful three year total shareholder return above 300% that signals longer term momentum is still very much intact even if sentiment has cooled recently.

If this kind of government backed space exposure has your attention, it could be worth exploring aerospace and defense stocks for other orbital and defense names riding similar structural tailwinds.

With revenue and earnings still growing double digits and the share price well below analyst targets, has MDA Space quietly slipped into undervalued territory, or is the market already baking in its next leg of growth?

Most Popular Narrative Narrative: 35.8% Undervalued

With the narrative fair value sitting well above MDA Space’s last close at CA$24.90, the story hinges on powerful multi year growth assumptions.

The ramp up of large LEO constellation contracts, including the landmark $1.8 billion EchoStar direct to device satellite order with options to expand, and multiple pipeline opportunities in broadband, defense, and IoT, is expected to drive robust multi year revenue growth as global demand for satellite connectivity accelerates.

Curious how that mega contract outlook turns into today’s fair value, despite moderated growth and margin expectations, and a higher future earnings multiple than the sector?

Result: Fair Value of $38.79 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside depends on flawless execution. Mega constellation delays or underutilised new capacity could quickly pressure margins and dampen sentiment.

Find out about the key risks to this MDA Space narrative.

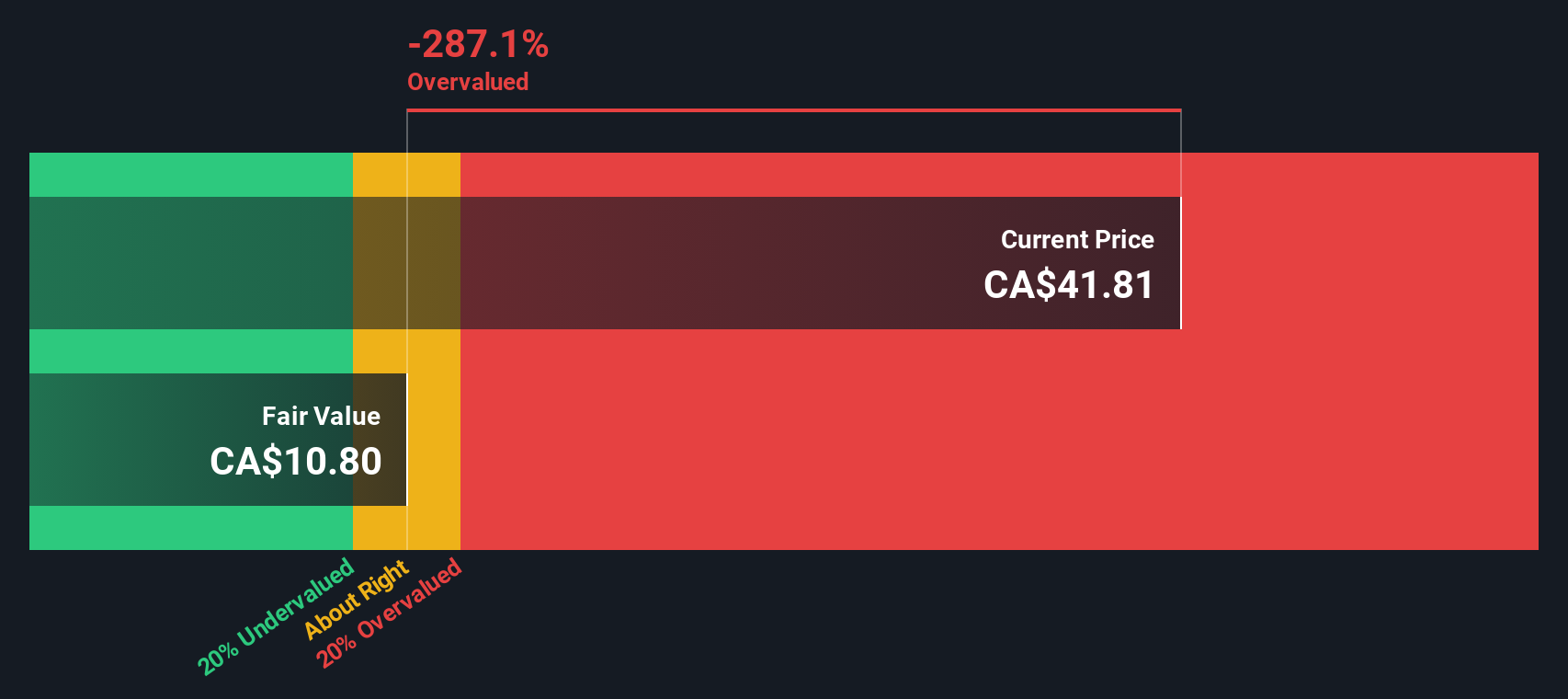

Another Angle on Valuation

Our DCF model paints a much cooler picture, suggesting fair value closer to CA$6.44, which would make MDA look expensive at today’s CA$24.90. Is the market correctly pricing near term cash flow risks, or underestimating MDA’s long term optionality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out MDA Space for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 902 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own MDA Space Narrative

If you see things differently or want to dig into the numbers yourself, you can build a custom view in minutes. Do it your way.

A great starting point for your MDA Space research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If MDA Space sparked your interest, do not stop here. Your next great opportunity could be sitting just a few clicks away in our stock screeners.

- Capitalize on mispricing by targeting companies trading below intrinsic value through these 902 undervalued stocks based on cash flows before the broader market catches on.

- Ride the innovation wave by focusing on fast moving automation and machine learning names using these 26 AI penny stocks built for growth oriented investors.

- Strengthen your income stream by zeroing in on reliable payers with attractive yields through these 15 dividend stocks with yields > 3% while payouts still look compelling.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:MDA

MDA Space

Provides space technology solutions and in Canada, the United States, Europe, Asia, the Middle East, and internationally.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

66 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

EN

Enemy on Halyk Bank of Kazakhstan ·

Halyk Bank of Kazakhstan will see revenue grow 11% as their future PE reaches 3.2x soon

Fair Value:US$52.2351.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

66 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative