Advertisement

Toronto-Dominion Bank (TSX:TD): Exploring Current Valuation After Strong Share Price Gains

Simply Wall St

Reviewed by Simply Wall St

Toronto-Dominion Bank (TSX:TD) shares have been gaining traction recently, sparking renewed interest from investors who are looking to assess the stock’s current valuation. Over the past month, TD’s price has climbed and this has reflected positive market sentiment.

See our latest analysis for Toronto-Dominion Bank.

After a strong run-up so far this year, Toronto-Dominion Bank’s share price is up 53% year to date and momentum has been building, boosted by solid quarterly results and steady investor confidence. The one-year total shareholder return stands at an impressive 54%, reflecting both price appreciation and dividends.

If you’re curious to see which other companies have been catching investors’ attention lately, you might want to broaden your search and discover fast growing stocks with high insider ownership

But with shares at a multi-year high and investor optimism running strong, the big question now is whether TD still offers value for new buyers or if the market has already priced in future growth.

Most Popular Narrative: 3.5% Overvalued

Toronto-Dominion Bank’s most followed narrative now puts fair value at CA$113.14, which is just above the last close of CA$117.06. This highlights a tight gap that frames TD's valuation as slightly stretched by recent optimism and profit strength.

Persistent investment in compliance, notably elevated AML remediation, cyber, and fraud prevention costs, is expected to drive higher structural expenses. This may weigh on net margins and overall earnings growth well into 2026 and 2027, as regulatory scrutiny and associated operational costs remain elevated.

Curious about what’s fueling the latest valuation bump? This narrative hinges on fierce cost pressures, shrinking margins, and ambitious earnings targets. Want to know which assumptions drive that fair value? There is a big story behind those numbers. Explore the surprising projections that shape this viewpoint.

Result: Fair Value of $113.14 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued revenue growth in core divisions and successful digital initiatives could support TD’s earnings outlook, even if broader market headwinds continue.

Find out about the key risks to this Toronto-Dominion Bank narrative.

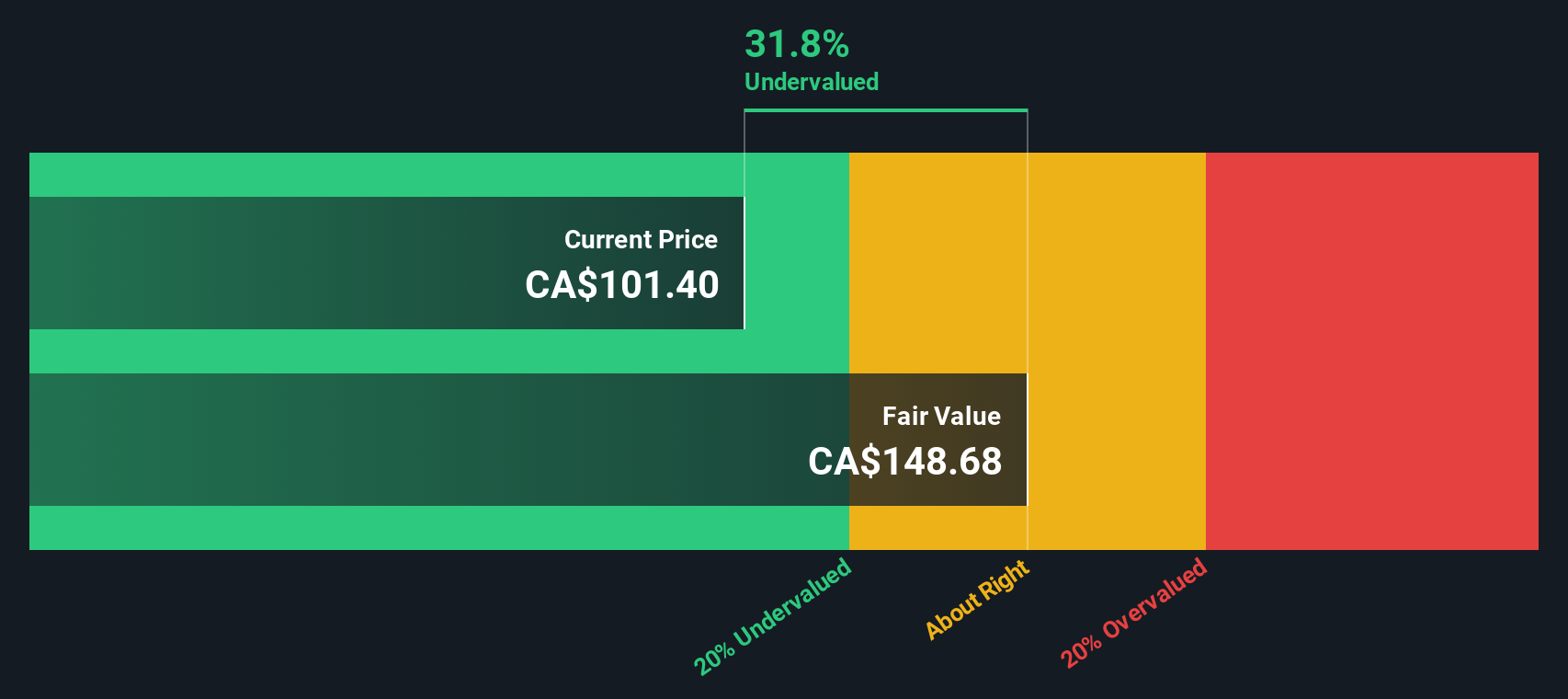

Another View: Our DCF Model Signals Deep Value

Looking at valuation from another angle, the SWS DCF model values Toronto-Dominion Bank at CA$161.98, well above the recent market price. This suggests shares could be significantly undervalued according to cash flow analysis, even as other perspectives argue the stock is pricey. Which model do you trust most?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Toronto-Dominion Bank Narrative

Not convinced by these numbers or want to take a hands-on approach? Crafting your own narrative takes just a few minutes. Dive into the details and Do it your way

A great starting point for your Toronto-Dominion Bank research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let your next big winner slip away. Uncover fresh opportunities across the market with ideas tailored to what’s working now. You may appreciate exploring these options.

- Capitalize on next-generation healthcare trends by reviewing these 30 healthcare AI stocks. These innovations are transforming patient outcomes with intelligent diagnostics and breakthrough medical technologies.

- Unlock high potential returns by evaluating these 3579 penny stocks with strong financials poised for breakout growth and hidden gems that are flying under the radar.

- Boost your portfolio’s income by picking these 15 dividend stocks with yields > 3%. These options consistently deliver yields above 3 percent and reward investors year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toronto-Dominion Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TD

Toronto-Dominion Bank

Provides various financial products and services in Canada, the United States, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative