Advertisement

- Canada

- /

- Oil and Gas

- /

- TSXV:HME

TSX Dividend Stocks To Consider In November 2025

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates through a period of AI-driven enthusiasm and valuation adjustments, recent job growth signals resilience in the economy despite global uncertainties. In such an environment, dividend stocks can offer stability and income potential, making them a compelling consideration for investors seeking balance amid fluctuating market sentiment.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Wajax (TSX:WJX) | 5.14% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.02% | ★★★★★☆ |

| Rogers Sugar (TSX:RSI) | 5.73% | ★★★★☆☆ |

| Pulse Seismic (TSX:PSD) | 16.73% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 3.65% | ★★★★★☆ |

| Olympia Financial Group (TSX:OLY) | 6.09% | ★★★★★☆ |

| National Bank of Canada (TSX:NA) | 3.00% | ★★★★★☆ |

| Great-West Lifeco (TSX:GWO) | 4.07% | ★★★★★☆ |

| Canadian Imperial Bank of Commerce (TSX:CM) | 3.26% | ★★★★★☆ |

| Bank of Montreal (TSX:BMO) | 3.76% | ★★★★★☆ |

Click here to see the full list of 17 stocks from our Top TSX Dividend Stocks screener.

We're going to check out a few of the best picks from our screener tool.

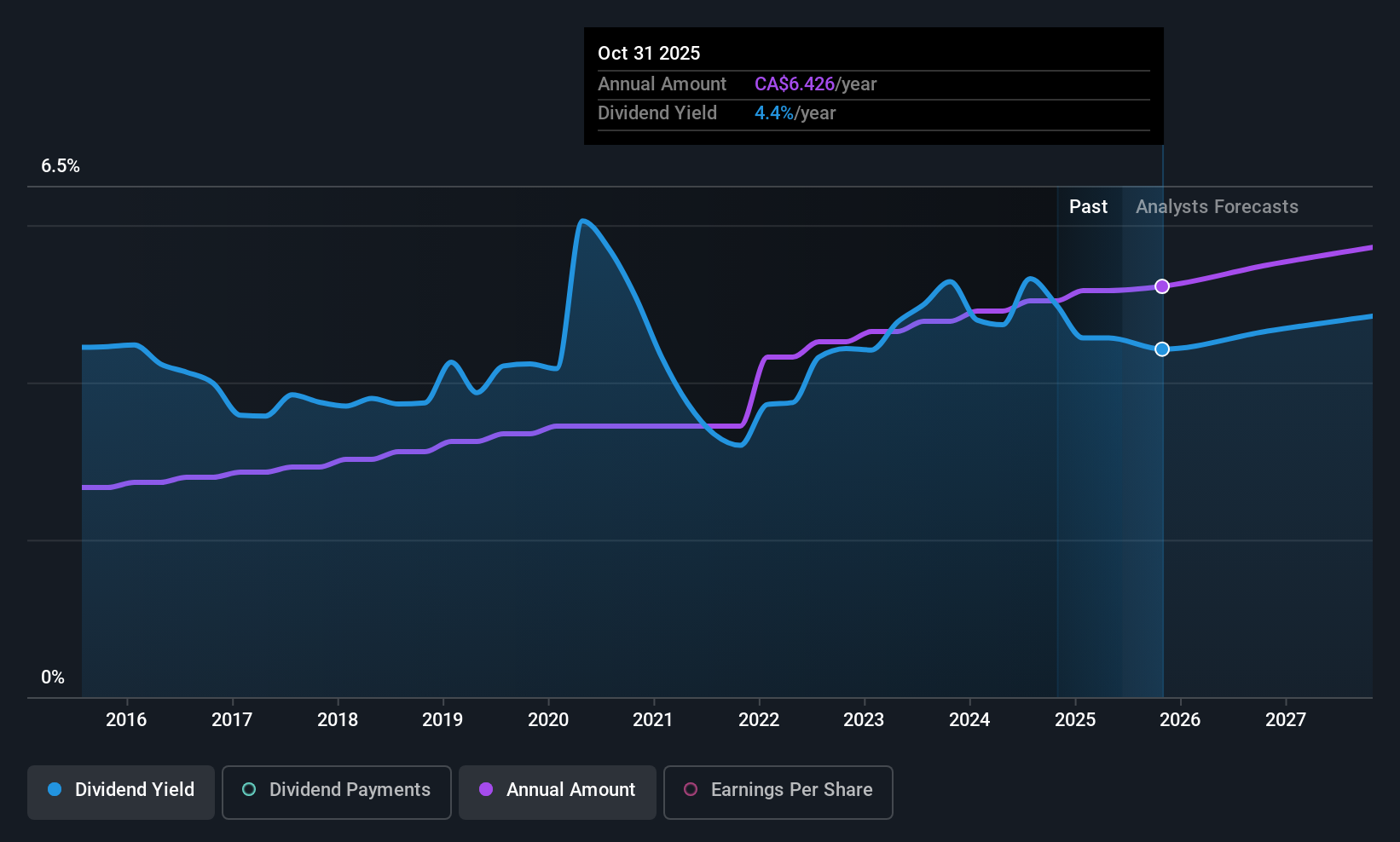

Bank of Montreal (TSX:BMO)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Bank of Montreal provides diversified financial services primarily in North America and has a market cap of CA$123.51 billion.

Operations: Bank of Montreal's revenue segments include Canadian Personal and Commercial Banking at CA$9.78 billion, U.S. Personal and Commercial Banking at CA$8.60 billion, BMO Capital Markets at CA$6.81 billion, and BMO Wealth Management at CA$6.19 billion.

Dividend Yield: 3.8%

Bank of Montreal's dividend payments have been stable and reliable over the past decade, supported by a reasonable payout ratio of 55.6%, ensuring sustainability. Although its current yield of 3.76% is below the top tier in Canada, dividends are well-covered by earnings and forecasted to remain so in three years with a lower payout ratio of 48.4%. Recent initiatives like BMO Credit Coach enhance customer engagement but don't directly impact dividend prospects.

- Click to explore a detailed breakdown of our findings in Bank of Montreal's dividend report.

- Insights from our recent valuation report point to the potential overvaluation of Bank of Montreal shares in the market.

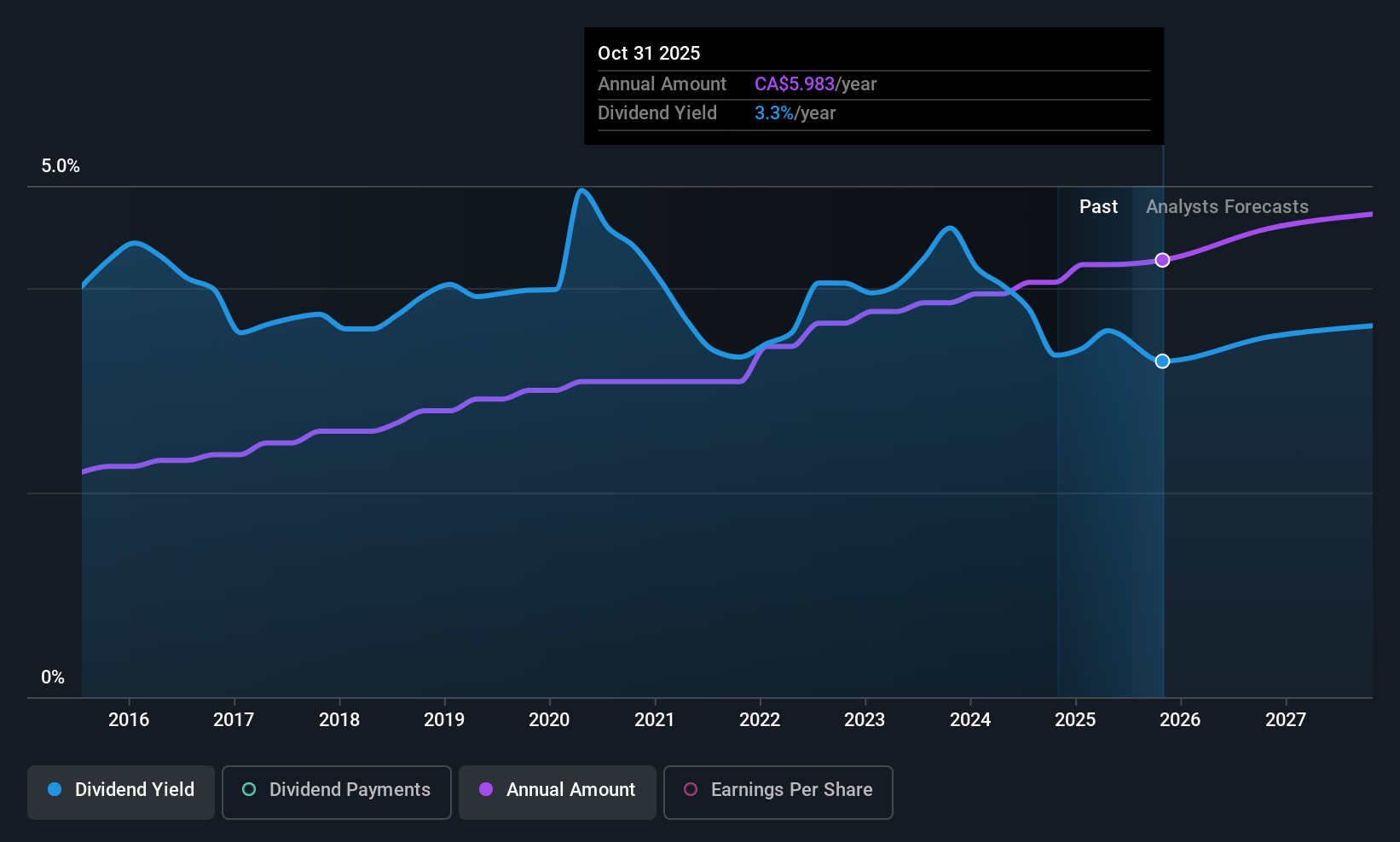

Royal Bank of Canada (TSX:RY)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Royal Bank of Canada operates as a diversified financial services company worldwide, with a market cap of CA$286.63 billion.

Operations: Royal Bank of Canada's revenue segments include Insurance (CA$1.39 billion), Capital Markets (CA$13.17 billion), Personal Banking (CA$17.27 billion), Wealth Management (CA$21.57 billion), and Commercial Banking (CA$6.94 billion).

Dividend Yield: 3%

Royal Bank of Canada offers a stable dividend yield of 3.02%, backed by a low payout ratio of 44.7%, ensuring dividends are well-covered and forecasted to remain sustainable in three years at 43.1%. While its yield is lower than the top Canadian payers, it has been reliable over the past decade with consistent growth. Recent fixed-income offerings, including senior unsecured notes, highlight ongoing capital management but don't directly affect dividend stability.

- Dive into the specifics of Royal Bank of Canada here with our thorough dividend report.

- Our valuation report unveils the possibility Royal Bank of Canada's shares may be trading at a premium.

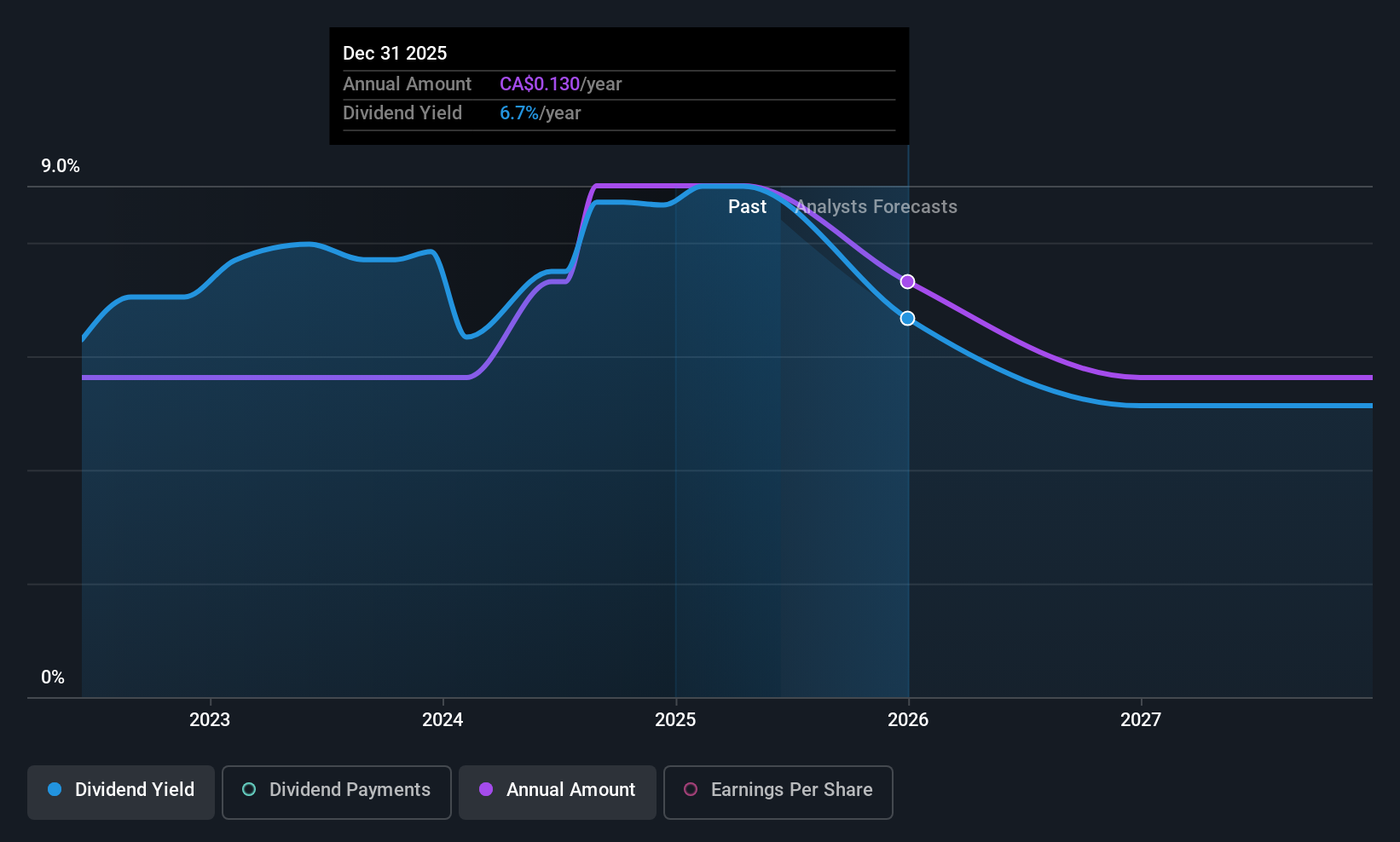

Hemisphere Energy (TSXV:HME)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Hemisphere Energy Corporation is involved in the acquisition, exploration, development, and production of petroleum and natural gas properties in Canada, with a market cap of CA$201.71 million.

Operations: Hemisphere Energy Corporation generates revenue from its petroleum and natural gas interests, amounting to CA$82.14 million.

Dividend Yield: 7.5%

Hemisphere Energy's dividend yield of 7.51% ranks in the top 25% of Canadian payers, with a payout ratio of 30.5%, indicating strong coverage by earnings and cash flows. Despite only three years of dividend history, payments have been stable. Recent financials show declining revenues and net income, with Q2 revenue at C$19.45 million down from C$22.66 million year-over-year, potentially impacting future growth prospects despite current value trading slightly below fair estimates.

- Navigate through the intricacies of Hemisphere Energy with our comprehensive dividend report here.

- Our valuation report here indicates Hemisphere Energy may be undervalued.

Key Takeaways

- Explore the 17 names from our Top TSX Dividend Stocks screener here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hemisphere Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:HME

Hemisphere Energy

Acquires, explores, develops, and produces petroleum and natural gas properties in Canada.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor