Advertisement

Should You Be Pleased About The CEO Pay At Elders Limited's (ASX:ELD)

Mark Allison became the CEO of Elders Limited (ASX:ELD) in 2014. This analysis aims first to contrast CEO compensation with other companies that have similar market capitalization. Then we'll look at a snap shot of the business growth. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. This method should give us information to assess how appropriately the company pays the CEO.

See our latest analysis for Elders

How Does Mark Allison's Compensation Compare With Similar Sized Companies?

Our data indicates that Elders Limited is worth AU$1.5b, and total annual CEO compensation was reported as AU$1.7m for the year to September 2019. We think total compensation is more important but we note that the CEO salary is lower, at AU$896k. When we examined a selection of companies with market caps ranging from AU$583m to AU$2.3b, we found the median CEO total compensation was AU$1.5m.

Now let's take a look at the pay mix on an industry and company level to gain a better understanding of where Elders stands. Talking in terms of the sector, salary represented approximately 56% of total compensation out of all the companies we analysed, while other remuneration made up 44% of the pie. Elders does not set aside a larger portion of remuneration in the form of salary, maintaining the same rate as the wider market.

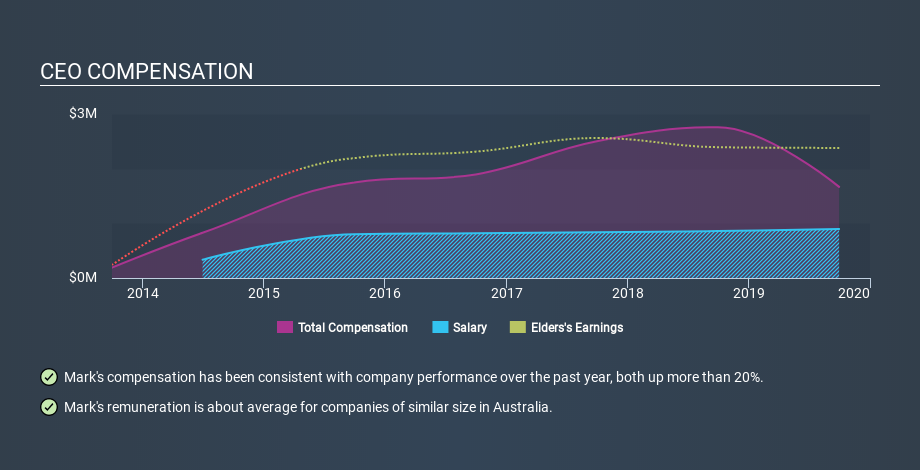

So Mark Allison is paid around the average of the companies we looked at. While this data point isn't particularly informative alone, it gains more meaning when considered with business performance. The graphic below shows how CEO compensation at Elders has changed from year to year.

Is Elders Limited Growing?

On average over the last three years, Elders Limited has shrunk earnings per share by 14% each year (measured with a line of best fit). It achieved revenue growth of 17% over the last year.

Few shareholders would be pleased to read that earnings per share are lower over three years. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that earnings per share has gone backwards over three years. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Shareholders might be interested in this free visualization of analyst forecasts.

Has Elders Limited Been A Good Investment?

Boasting a total shareholder return of 96% over three years, Elders Limited has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Mark Allison is paid around the same as most CEOs of similar size companies.

The company isn't growing earnings per share, but shareholder returns have been strong over the last three years. So we doubt many are complaining about the fairly normal CEO pay. Shifting gears from CEO pay for a second, we've spotted 2 warning signs for Elders you should be aware of, and 1 of them makes us a bit uncomfortable.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ASX:ELD

Elders

Engages in the provision of agricultural products and services to rural and regional customers primarily in Australia.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

61 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

61 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative