Advertisement

- Australia

- /

- Construction

- /

- ASX:LYL

Undiscovered Gems in Australia to Explore This August 2025

Simply Wall St

Reviewed by Simply Wall St

As the Australian market navigates a sea of mixed signals, with futures looking uncertain amidst a backdrop of robust U.S. economic growth and fluctuating commodity prices, investors are keenly evaluating the latest earnings reports to gauge potential opportunities. In this dynamic environment, identifying promising small-cap stocks requires a focus on companies with strong fundamentals that can adapt to both local and global economic shifts.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.78% | 4.30% | ★★★★★★ |

| Fiducian Group | NA | 10.00% | 9.57% | ★★★★★★ |

| Spheria Emerging Companies | NA | -1.31% | 0.28% | ★★★★★★ |

| Euroz Hartleys Group | NA | 1.82% | -25.32% | ★★★★★★ |

| Hearts and Minds Investments | NA | 56.27% | 59.19% | ★★★★★★ |

| Red Hill Minerals | NA | 95.16% | 40.06% | ★★★★★★ |

| Djerriwarrh Investments | 2.39% | 8.18% | 7.91% | ★★★★★★ |

| Zimplats Holdings | 5.44% | -9.79% | -42.03% | ★★★★★☆ |

| Peet | 53.46% | 12.70% | 31.21% | ★★★★☆☆ |

| Australian United Investment | 1.90% | 5.23% | 4.56% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

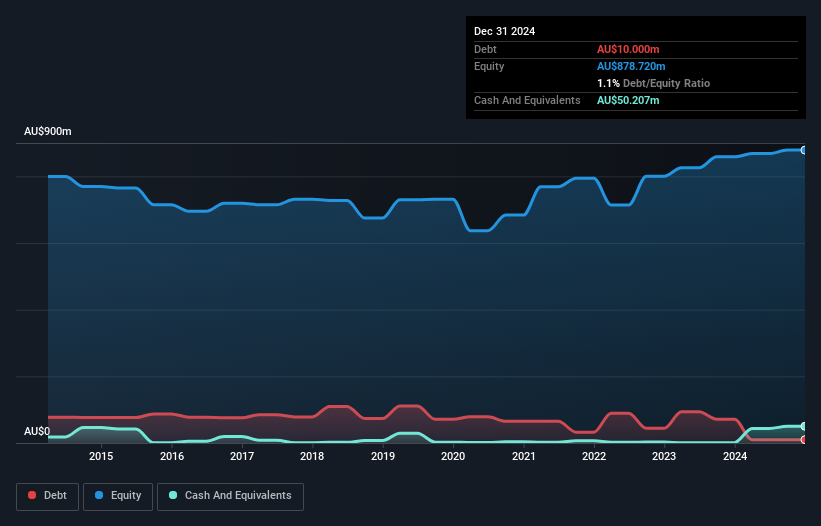

Djerriwarrh Investments (ASX:DJW)

Simply Wall St Value Rating: ★★★★★★

Overview: Djerriwarrh Investments Limited is a publicly owned investment manager with a market cap of A$828.26 million.

Operations: Djerriwarrh Investments generates revenue primarily through its portfolio of investments, amounting to A$53.07 million.

Djerriwarrh Investments, a notable player in Australia's financial landscape, showcases robust fundamentals. Over the past five years, its earnings have grown by 7.9% annually, supported by a reduced debt-to-equity ratio from 12.3% to 2.4%. The company has high-quality earnings and maintains a price-to-earnings ratio of 21.1x, undercutting the industry average of 22.5x. Recent financials reveal net income at A$39.18 million for fiscal year ending June 2025 with basic EPS slightly up at A$0.1487 from A$0.1485 last year, reflecting stability amidst modest revenue changes to A$53 million from A$53.38 million prior year.

- Click to explore a detailed breakdown of our findings in Djerriwarrh Investments' health report.

Gain insights into Djerriwarrh Investments' past trends and performance with our Past report.

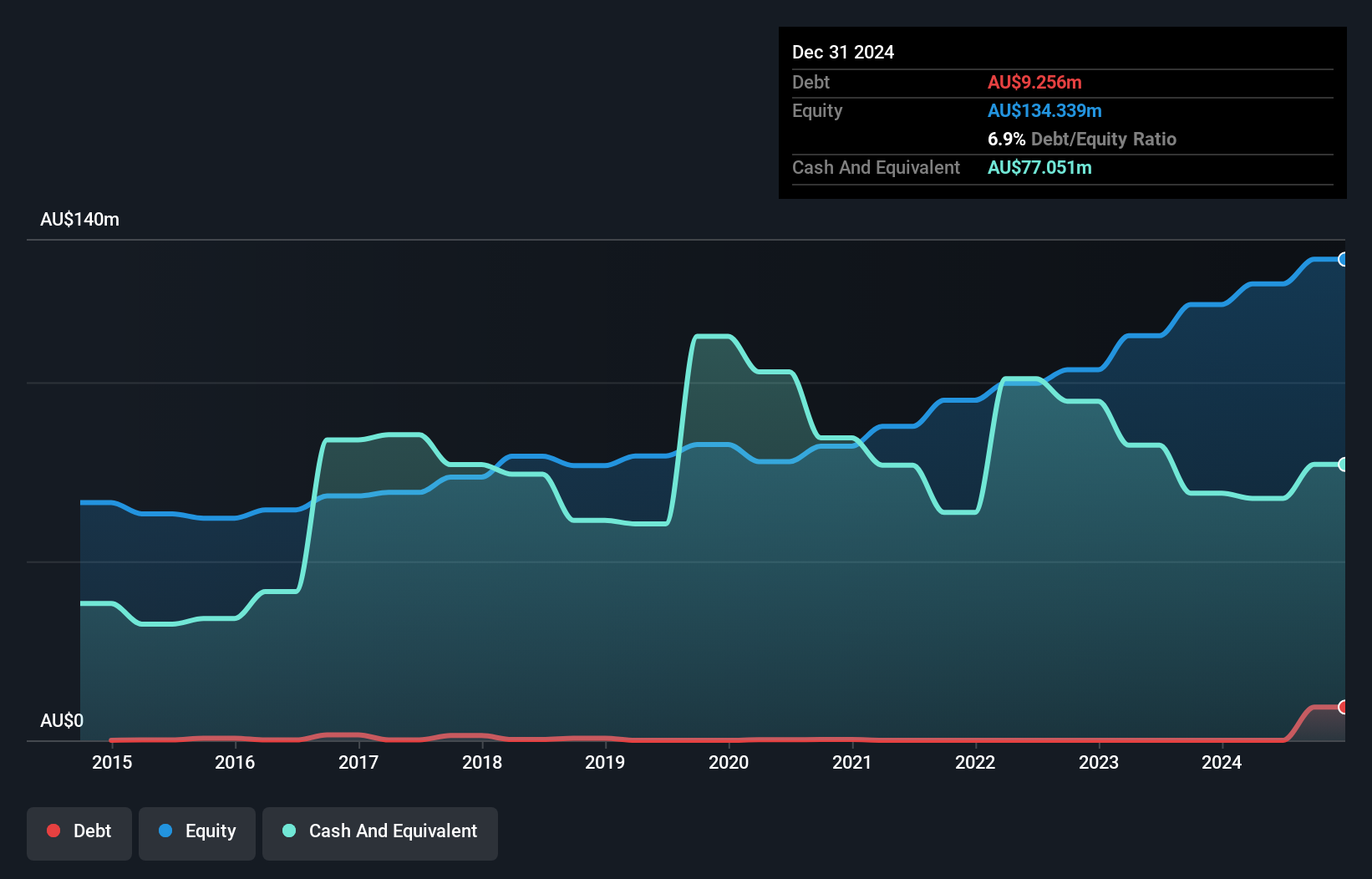

Lycopodium (ASX:LYL)

Simply Wall St Value Rating: ★★★★★☆

Overview: Lycopodium Limited is an Australian company offering engineering and project delivery services across the resources, rail infrastructure, and industrial processes sectors, with a market capitalization of A$462.32 million.

Operations: Lycopodium's primary revenue stream is from the resources sector, generating A$342.76 million, with additional contributions from rail infrastructure and process industries at A$11.03 million and A$10.08 million respectively.

Lycopodium, a nimble player in the engineering sector, trades at 60.7% below its estimated fair value, hinting at potential upside. Despite high-quality earnings and positive free cash flow of A$30.77 million as of September 2024, recent performance saw a dip with net income dropping to A$42.22 million from A$50.71 million the previous year. The debt-to-equity ratio has risen to 1% over five years but remains manageable given their cash position surpasses total debt levels. While revenue is forecasted to grow by 8.12% annually, significant insider selling recently might raise some eyebrows among investors considering its future prospects.

- Dive into the specifics of Lycopodium here with our thorough health report.

Review our historical performance report to gain insights into Lycopodium's's past performance.

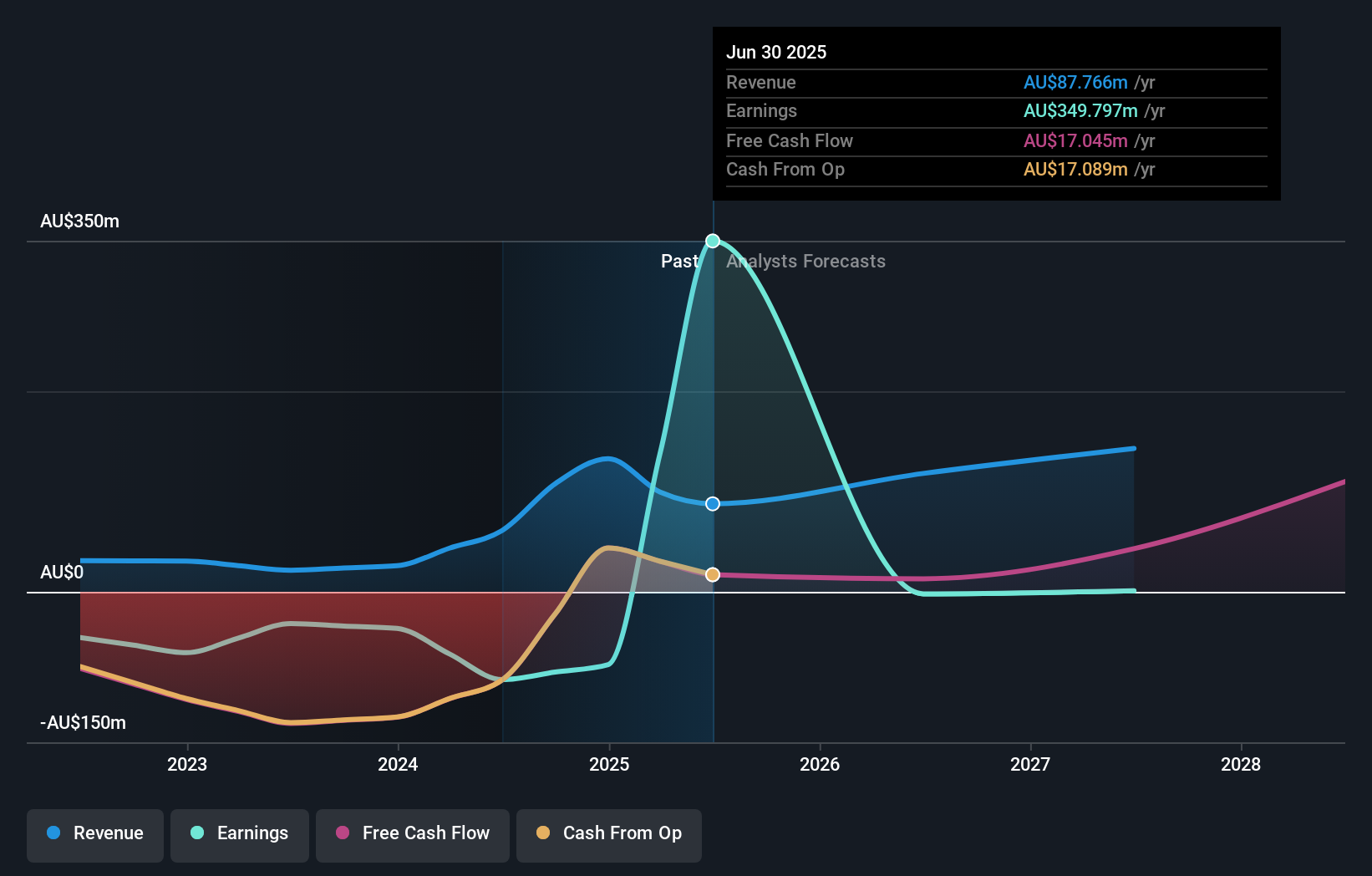

Omni Bridgeway (ASX:OBL)

Simply Wall St Value Rating: ★★★★★☆

Overview: Omni Bridgeway Limited, along with its subsidiaries, offers dispute and litigation finance services across various global regions including Australia, the United States, Canada, Latin America, Asia, New Zealand, Europe, the Middle East, and Africa; it has a market capitalization of A$465.82 million.

Operations: Omni Bridgeway generates revenue primarily from funding and providing services related to legal dispute resolution, amounting to A$770.40 million. The company's net profit margin is a key financial metric to consider when analyzing its profitability.

Omni Bridgeway, a notable player in the financial sector, has shown impressive growth with net income soaring to A$349.8 million from a loss of A$87.52 million last year. Its revenue jumped significantly to A$651.22 million from A$184.59 million, highlighting robust performance despite sales dropping to A$54.99 million from A$71.05 million previously. The company has reduced its debt-to-equity ratio dramatically over five years, now standing at 2.3% compared to 18.7%. With a price-to-earnings ratio of 1.3x against the market's 19.6x and more cash than total debt, Omni Bridgeway appears well-positioned in its industry despite forecasts suggesting earnings might decline by an average of 148% annually over the next three years while revenue is expected to grow by nearly 24% per year.

- Click here and access our complete health analysis report to understand the dynamics of Omni Bridgeway.

Examine Omni Bridgeway's past performance report to understand how it has performed in the past.

Next Steps

- Click this link to deep-dive into the 53 companies within our ASX Undiscovered Gems With Strong Fundamentals screener.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:LYL

Lycopodium

Provides engineering and project delivery services in the resources, rail infrastructure, and industrial processes sectors in Australia.

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor