Advertisement

- Australia

- /

- Diversified Financial

- /

- ASX:HLI

Undiscovered Gems in Australia to Explore This November 2025

Simply Wall St

Reviewed by Simply Wall St

As the Australian market grapples with a downturn, highlighted by a predicted 1.4% drop in the ASX 200 and broader economic uncertainties following the U.S. shutdown, investors are navigating a landscape marked by both caution and opportunity. In such an environment, identifying promising stocks involves looking for companies that demonstrate resilience and potential growth despite prevailing market challenges.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 10.00% | 9.57% | ★★★★★★ |

| Spheria Emerging Companies | NA | -1.31% | 0.28% | ★★★★★★ |

| Hearts and Minds Investments | NA | 56.27% | 59.19% | ★★★★★★ |

| Euroz Hartleys Group | NA | 1.82% | -25.32% | ★★★★★★ |

| Djerriwarrh Investments | 2.39% | 8.18% | 7.91% | ★★★★★★ |

| Focus Minerals | NA | 75.35% | 51.34% | ★★★★★★ |

| Energy World | NA | -47.50% | -44.86% | ★★★★★☆ |

| Zimplats Holdings | 5.44% | -9.79% | -42.03% | ★★★★★☆ |

| Peet | 53.46% | 12.70% | 31.21% | ★★★★☆☆ |

| Australian United Investment | 1.90% | 5.23% | 4.56% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

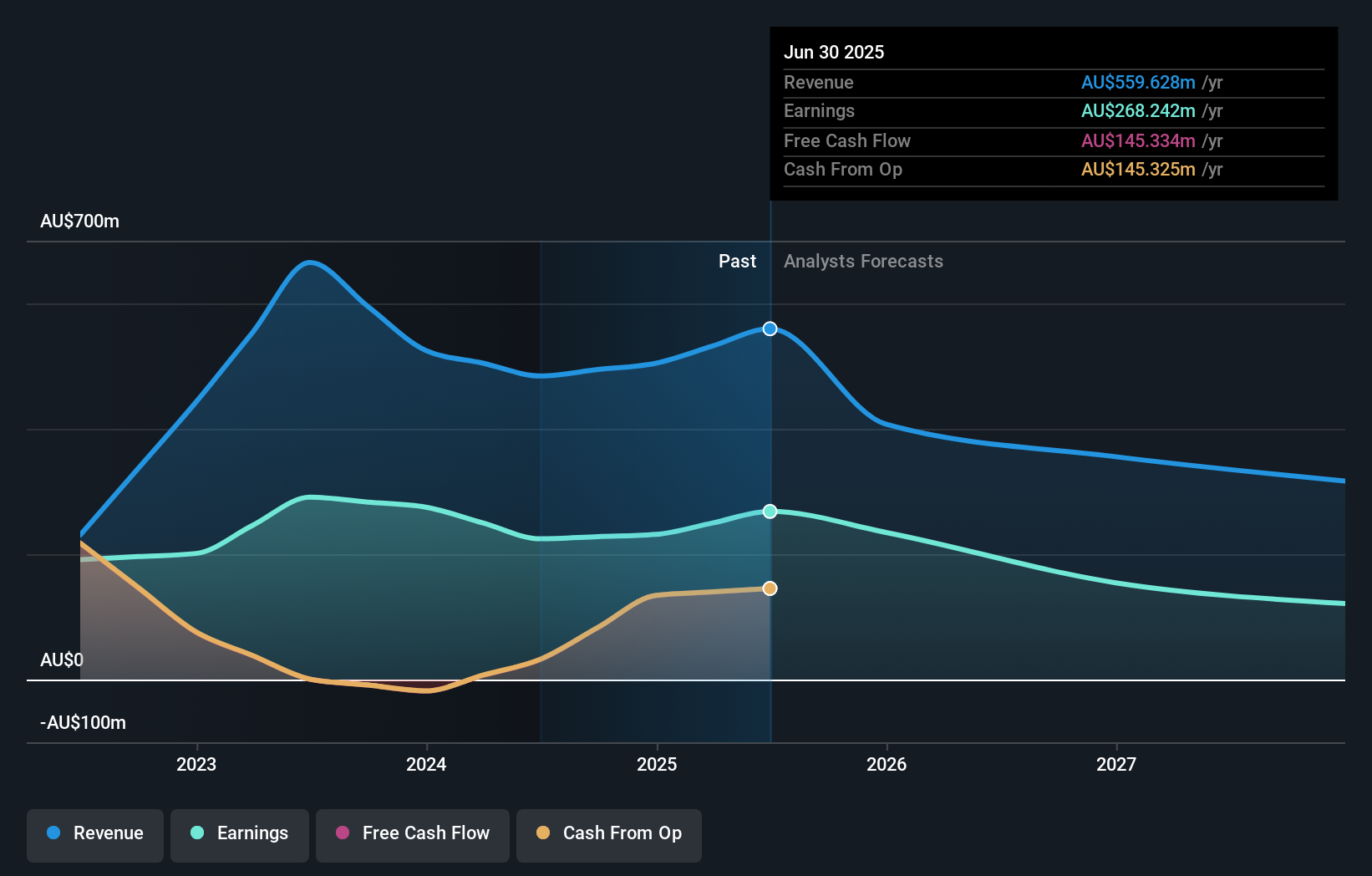

Helia Group (ASX:HLI)

Simply Wall St Value Rating: ★★★★★☆

Overview: Helia Group Limited, along with its subsidiaries, operates in the loan mortgage insurance sector mainly in Australia and has a market capitalization of A$1.60 billion.

Operations: Helia generates revenue primarily from its loan mortgage insurance business, amounting to A$559.63 million. The company's financial performance is influenced by its net profit margin trends.

Helia Group, a smaller player in the Australian financial landscape, is trading at 66.9% below its estimated fair value and offers good relative value compared to peers. Despite recent earnings growth of 19.4%, surpassing the industry average, future prospects appear challenging with an anticipated annual revenue decrease of 18.9% over three years due to client losses and policy changes like the Home Guarantee Scheme expansion. The company's net income for the first half of 2025 was A$133.7 million, up from A$97 million last year, yet profit margins are expected to drop from 47.9% to 34.7%. Helia's market share and capital strength offer some stability amidst these pressures; however, heavy dividend payouts could limit reinvestment opportunities crucial for sustaining competitiveness in a shifting market environment.

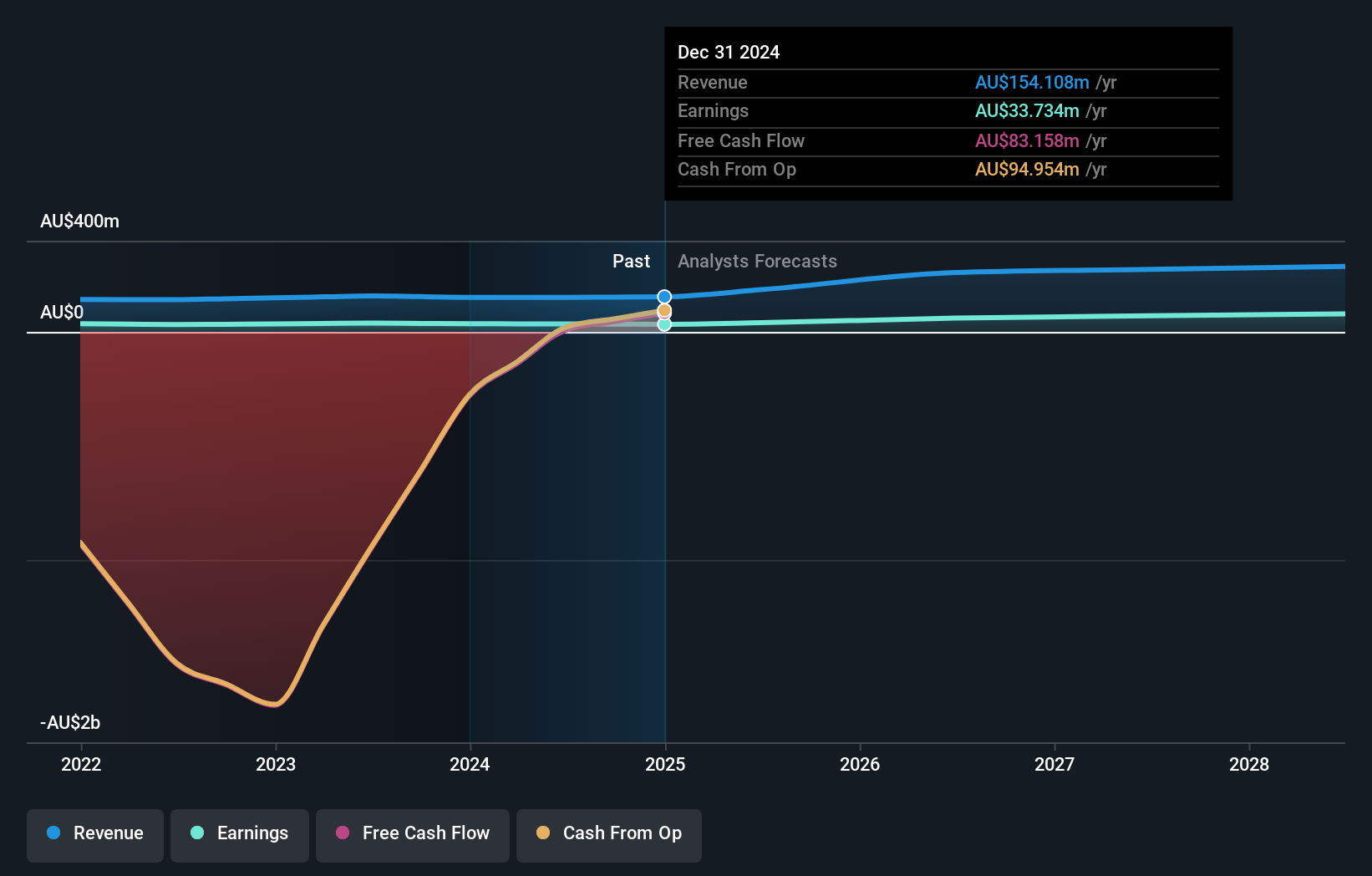

MyState (ASX:MYS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: MyState Limited operates in Australia, offering banking, trustee, equipment finance, and managed fund products and services through its subsidiaries, with a market capitalization of A$736.44 million.

Operations: MyState Limited generates revenue primarily from its MyState Bank segment, contributing A$140.27 million, and also earns from Wealth Management at A$14.82 million and Auswide Bank (including Selfco) at A$30.98 million. The net profit margin provides insight into the company's profitability relative to total revenue streams across its segments.

With total assets of A$15.3B and equity at A$736M, MyState stands out in the banking sector with a focus on low-risk funding sources, as 76% of liabilities are customer deposits. The bank's total loans amount to A$13.2B, with an appropriate bad loan ratio of 0.7%, but it has a low allowance for these loans at 14%. Earnings grew by 0.8% last year, surpassing the industry average, and future growth is projected at an impressive 16.2% annually. However, significant shareholder dilution occurred recently despite promising merger synergies and digital upgrades enhancing operational efficiency and user experience.

SHAPE Australia (ASX:SHA)

Simply Wall St Value Rating: ★★★★★★

Overview: SHAPE Australia Corporation Limited, along with its subsidiaries, operates in the construction, fitout, and refurbishment sector for commercial properties across Australia with a market cap of A$533.59 million.

Operations: SHAPE Australia's primary revenue stream is from its heavy construction segment, generating A$956.87 million. The company's market cap stands at A$533.59 million.

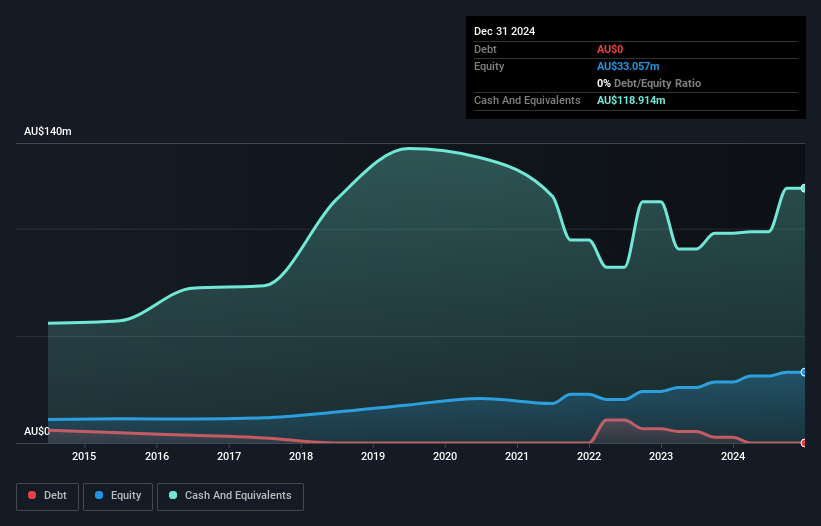

SHAPE Australia, a nimble player in the construction sector, has seen its earnings grow by 31.9% over the past year, outpacing industry norms. Trading at A$4.24 per share, it sits 19.3% below its estimated fair value of A$5.27, suggesting potential upside for investors willing to consider its prospects amidst challenges like competitive pressures and reliance on office fit-outs. The company is debt-free and boasts high-quality earnings with a focus on sustainability and digital innovation to enhance margins currently at 2.2%. Recent board changes aim to bolster M&A capabilities as part of their growth strategy moving forward.

Seize The Opportunity

- Gain an insight into the universe of 56 ASX Undiscovered Gems With Strong Fundamentals by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Helia Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:HLI

Helia Group

Helia Group Limited, together with its subsidiaries, is involved in the loan mortgage insurance business primarily in Australia.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor