- United States

- /

- Airlines

- /

- NasdaqGS:UAL

United Airlines Holdings (UAL) Reports Q2 Earnings, Completes US$681 Million Buyback

Reviewed by Simply Wall St

United Airlines Holdings (UAL) recently reported its second-quarter results, showing revenue growth but a decline in net income. Despite this, the company's stock experienced a significant 33% increase over the last quarter. The revenue boost might have added weight to its stock performance, aligning with broader market trends where the S&P 500 and Nasdaq were on track for record highs. Additionally, United's ongoing share buyback program signifies a commitment to shareholder value, enhancing its appeal in a competitive and optimistic market landscape amidst collaborative efforts with JetBlue and internal product developments.

The recent surge in United Airlines Holdings' (UAL) share price, up 33% last quarter despite a drop in net income, highlights the market's optimistic view of its revenue growth and strategic share buyback initiatives. This aligns with a broader market trend, as both the S&P 500 and Nasdaq approach record highs. Such developments resonate with United’s focus on increasing brand loyalty and customer experience through enhancements like new lounges and upgraded WiFi, likely to further drive revenue and bolster earnings. However, the existing economic uncertainties could still impart risks to this positive outlook.

Over a five-year period, United Airlines has delivered a very large total return of 179.35%, underscoring its resilient growth trajectory even in the face of industry volatility. In comparison over the past year, United's performance surpassed both the US Market's 10% return and the US Airlines industry's 36.1% increase, reflecting its strong positioning within the sector.

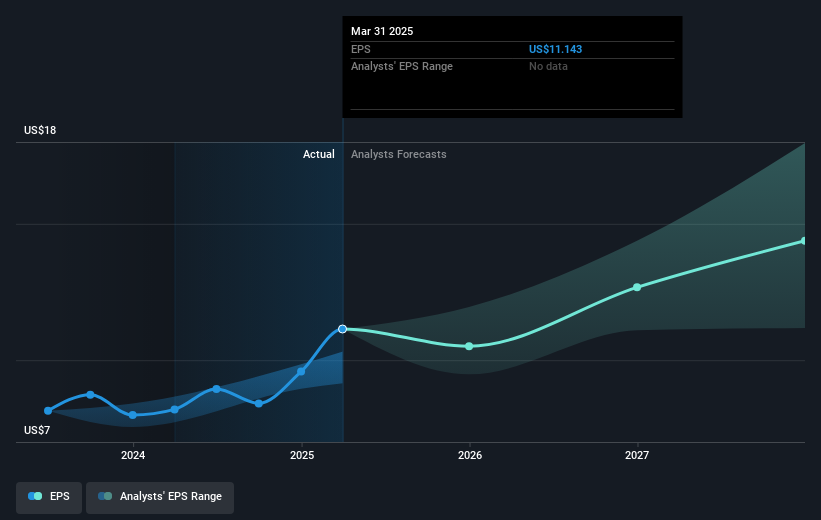

The consensus price target for UAL is US$96.29, representing a potential uplift from the current share price of US$88.47. This suggests further room for growth based on analysts' future revenue expectations, which assume annual growth of 4.8% over the next three years, and projected earnings of US$4.1 billion by 2028. However, achieving these targets hinges on navigating risks such as softer travel demand and economic uncertainty, which could adversely impact revenue forecasts and profitability. The current price position relative to the target suggests market confidence in the company’s strategic direction and potential for share value enhancement.

Understand United Airlines Holdings' earnings outlook by examining our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:UAL

United Airlines Holdings

Through its subsidiaries, provides air transportation services in the United States, Canada, Atlantic, the Pacific, and Latin America.

Proven track record and fair value.

Similar Companies

Market Insights

Community Narratives