Advertisement

- United Kingdom

- /

- Chemicals

- /

- LSE:ESNT

UK Market: Unveiling 3 Stocks That May Be Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 index recently experienced a downturn due to weak trade data from China, market participants are closely watching global economic indicators that could impact investment decisions. In such an environment, identifying stocks that may be trading below their estimated value can offer potential opportunities for investors looking to navigate these uncertain times.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Victorian Plumbing Group (AIM:VIC) | £0.678 | £1.29 | 47.5% |

| ProCook Group (LSE:PROC) | £0.30 | £0.56 | 46.8% |

| Pan African Resources (LSE:PAF) | £0.918 | £1.83 | 49.9% |

| PageGroup (LSE:PAGE) | £2.338 | £4.52 | 48.3% |

| Forterra (LSE:FORT) | £1.73 | £3.23 | 46.4% |

| Essentra (LSE:ESNT) | £0.931 | £1.70 | 45.3% |

| Begbies Traynor Group (AIM:BEG) | £1.12 | £2.20 | 49% |

| Barratt Redrow (LSE:BTRW) | £3.788 | £7.43 | 49% |

| Airtel Africa (LSE:AAF) | £3.05 | £5.87 | 48% |

| Advanced Medical Solutions Group (AIM:AMS) | £2.095 | £4.16 | 49.6% |

Here's a peek at a few of the choices from the screener.

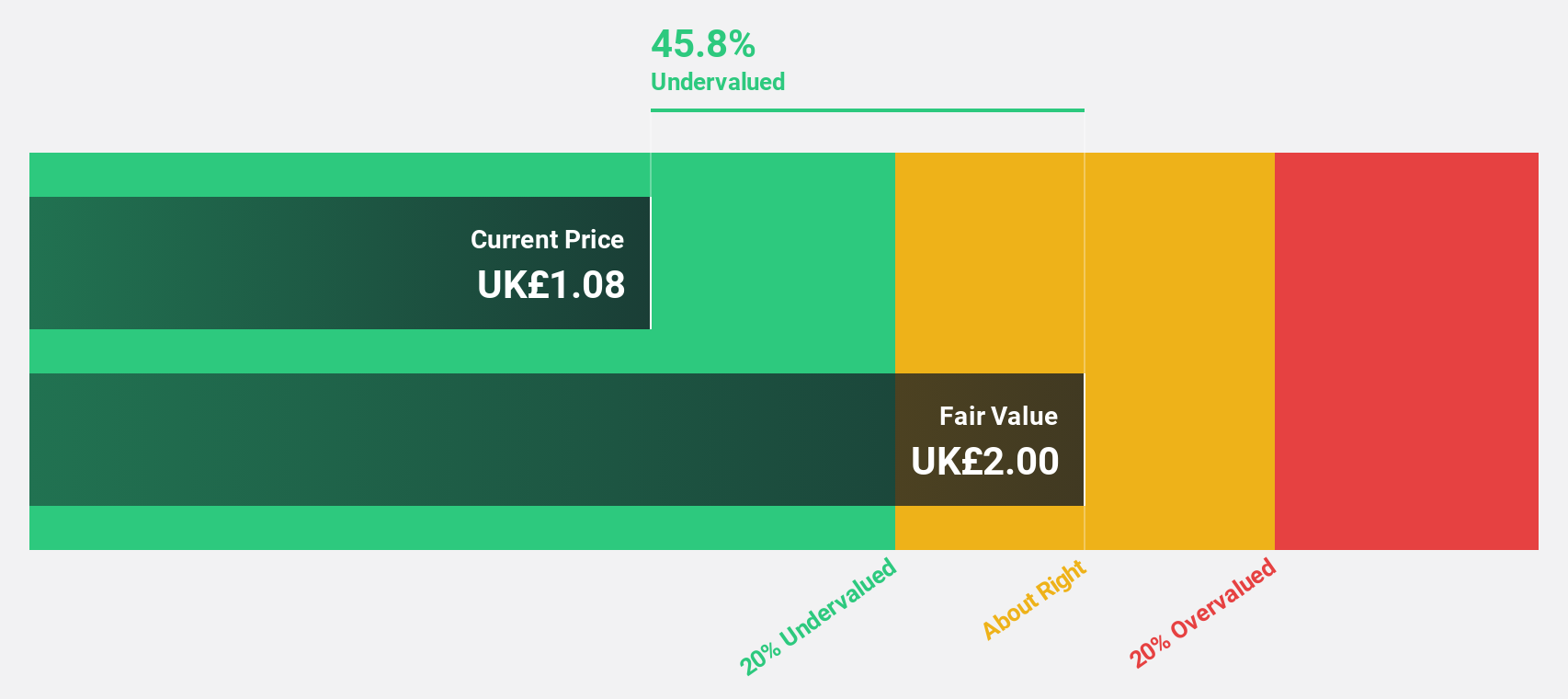

Barratt Redrow (LSE:BTRW)

Overview: Barratt Redrow plc operates in the housebuilding sector within the United Kingdom and has a market capitalization of approximately £5.36 billion.

Operations: The company's revenue is primarily derived from its housebuilding segment, which generated £5.58 billion.

Estimated Discount To Fair Value: 49%

Barratt Redrow is trading at a significant discount, with its stock price 49% below estimated fair value and more than 20% undervalued based on discounted cash flow analysis. Despite recent executive changes, the company reported strong financial results with sales of £5.58 billion and net income of £186.4 million for the year ending June 2025. However, its dividend yield of 4.65% is not well covered by earnings or free cash flows, indicating potential sustainability concerns.

- Upon reviewing our latest growth report, Barratt Redrow's projected financial performance appears quite optimistic.

- Take a closer look at Barratt Redrow's balance sheet health here in our report.

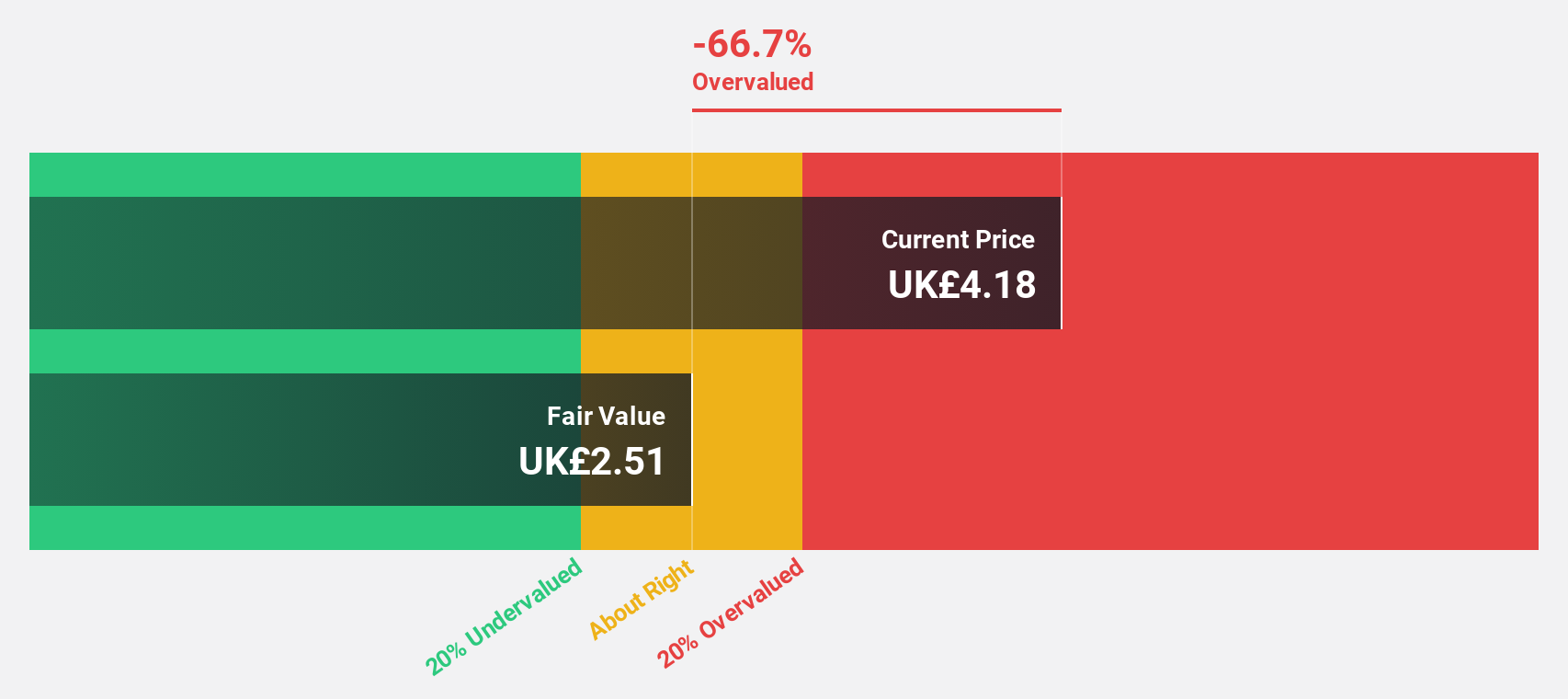

Essentra (LSE:ESNT)

Overview: Essentra plc manufactures and distributes plastic injection moulded, vinyl dip moulded, and metal items across Europe, the Middle East, Africa, the Americas, and the Asia Pacific with a market cap of £265.58 million.

Operations: Essentra's revenue is derived from its operations in manufacturing and distributing plastic injection moulded, vinyl dip moulded, and metal items across various regions including Europe, the Middle East, Africa, the Americas, and the Asia Pacific.

Estimated Discount To Fair Value: 45.3%

Essentra is trading at a substantial discount, with its price 45.3% below fair value and significantly undervalued based on discounted cash flow analysis. Despite large one-off items affecting results, earnings surged by a very large amount last year and are projected to grow 38.4% annually, outpacing the UK market's growth rate of 14.5%. However, revenue growth is modest at 4.8%, and return on equity is expected to remain low at 8.4%.

- Insights from our recent growth report point to a promising forecast for Essentra's business outlook.

- Dive into the specifics of Essentra here with our thorough financial health report.

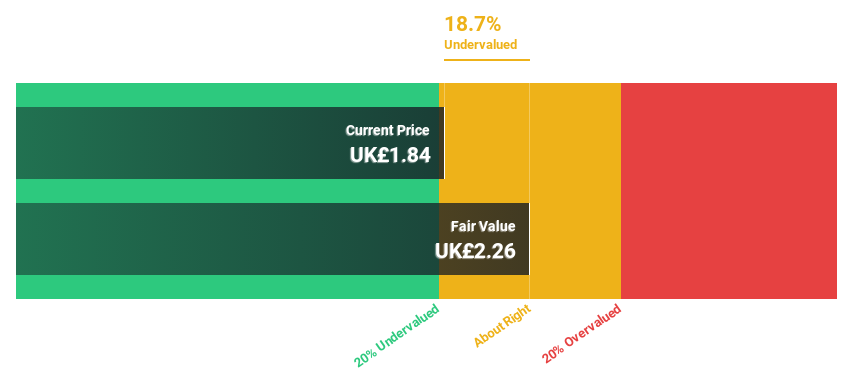

Wickes Group (LSE:WIX)

Overview: Wickes Group plc is a UK-based retailer specializing in home improvement products and services, with a market cap of approximately £507.79 million.

Operations: The company generates revenue from its operations in the UK through the retail of home improvement products and services, amounting to £1.58 billion.

Estimated Discount To Fair Value: 29.7%

Wickes Group is significantly undervalued, trading 29.7% below its estimated fair value of £3.08 per share, based on discounted cash flow analysis. Despite large one-off items impacting financials, earnings are forecast to grow at a robust 25.1% annually, surpassing the UK market's growth rate of 14.5%. However, revenue growth remains modest at 4.5%, and its dividend yield of 5.02% is not well covered by earnings, posing potential sustainability concerns.

- The analysis detailed in our Wickes Group growth report hints at robust future financial performance.

- Navigate through the intricacies of Wickes Group with our comprehensive financial health report here.

Make It Happen

- Gain an insight into the universe of 53 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Essentra might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:ESNT

Essentra

Engages in the manufacturing and distribution of plastic injection moulded, vinyl dip moulded, and metal items in Europe, the Middle East, Africa, the Americas, and the Asia Pacific.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

96 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative