Last Update 25 Jun 26

Fair value Increased 0.48%BKH: Merger With NorthWestern And Data Center Projects Are Expected To Support Returns

Analysts have nudged their average fair value estimate for Black Hills slightly higher to about $83 from roughly $83, pointing to a series of recent price target increases that highlight perceived benefits from the pending all stock merger, including greater scale, a stronger balance sheet, broader jurisdictional diversity, and an expanded infrastructure pipeline across data centers, transmission, generation, and gas.

Analyst Commentary

Recent research around Black Hills centers on how the pending all stock merger could influence valuation, balance sheet strength, and growth opportunities tied to regulated infrastructure projects.

Bullish Takeaways

- Bullish analysts highlight the pending merger with NorthWestern Energy as a key support for their fair value work. They point to the combined scale and broader jurisdictional mix as positives for earnings durability and regulatory risk spreading.

- The larger balance sheet expected after the merger is seen as helpful for funding a bigger capital program across data centers, transmission, generation, and gas infrastructure, without relying solely on more expensive sources of capital.

- Recent upward adjustments to fair value estimates are tied to what bullish analysts view as an underappreciated infrastructure pipeline. The merger is framed as a way to lengthen the runway of regulated projects that can support long term rate base growth.

- Initiation and upgrades in the coverage universe signal growing interest in Black Hills as a potential beneficiary of increased data center power needs and grid investment, provided the company can execute its capital plans on time and within approved regulatory frameworks.

Bearish Takeaways

- More cautious analysts focus on execution risk around the all stock merger, including the need to secure timely approvals and integrate operations without cost overruns or delays that could weigh on returns.

- There is also attention on regulatory uncertainty, as a larger multi state footprint can introduce complexity around rate cases, allowed returns, and political scrutiny of future infrastructure spending.

- Some investors may worry that a bigger capital pipeline in data centers, transmission, and generation could face scheduling, permitting, or cost pressures that affect cash flows if not carefully managed.

- Skeptics also point out that any merger driven rerating of Black Hills shares depends on the combined company hitting its targeted synergies and capital allocation plans. These outcomes are still unproven until the transaction is completed and integrated over time.

What’s in the News for Black Hills

- Bank of America upgraded Black Hills to Buy and raised its price target, citing the pending all stock merger with NorthWestern Energy as a key factor. The firm highlighted expectations of greater scale, a stronger balance sheet, broader geographic diversification, and more infrastructure opportunities, including Wyoming data center growth potential (source: Bank of America coverage).

- Black Hills filed a rate review application with the Colorado Public Utilities Commission seeking a US$26.7 million annual revenue increase for its Colorado electric utility to recover about US$184 million of investments in reliability, grid strength, and generation life extension, with implementation targeted for the first quarter of 2027 (source: Colorado rate review filing).

- Black Hills shares fell 6.1% in recent trading during a period of broader utility sector weakness, with investors reacting to a refreshed at the market equity issuance program that could add share supply, even as Bank of America issued its Buy upgrade and US$78 price target tied to the planned NorthWestern Energy merger (source: market trading updates and analyst research).

- Black Hills is advancing a proposed 1.8 gigawatt data center project in Cheyenne, Wyoming, targeting service commencement in early 2028. The company is working directly with a potential large load customer that has provided more than US$200 million in refundable construction contributions and supporting agreements for generation equipment and a new substation (sources: company project update, Wyoming filings).

- At a special meeting of shareholders on April 2, 2026, Black Hills investors approved amendments to the company’s restated articles of incorporation, reflecting corporate governance changes linked to its longer term plans (source: shareholder meeting results).

Valuation Changes for Black Hills

Recent model tweaks around Black Hills focus on fine tuning rather than sweeping shifts, with small adjustments to fair value, profitability, and valuation multiples.

- Fair Value: The average fair value estimate has moved marginally to about $83.40 from roughly $83.00, reflecting a very small upward recalibration.

- Discount Rate: The discount rate assumption is effectively unchanged at about 7.11%, indicating a stable required return input in current models.

- Revenue Growth: The modeled long term revenue growth rate remains around 16.80%, with only a minimal numerical refinement that does not signal a directional shift.

- Net Profit Margin: The projected net profit margin stays close to 15.88%, with only a slight technical adjustment to the underlying figure.

- Future P/E: The forward P/E multiple used in some estimates has edged up slightly to about 15.24x from roughly 15.17x, indicating a small change in how Black Hills earnings are being valued in these models.

Key Takeaways

- Growing demand from tech-driven customers and regional development is accelerating volumetric growth and supporting long-term revenue expansion.

- Major capital investments and innovative regulatory strategies are strengthening earnings, cash flow stability, and future margins above industry averages.

- Heavy infrastructure investment and reliance on concentrated, volatile customer segments make Black Hills vulnerable to regulatory delays, evolving energy trends, and regional or environmental risks.

Catalysts

About Black Hills- Through its subsidiaries, operates as an electric and natural gas utility company in the United States.

- Accelerated demand growth from hyperscale data center and blockchain customers-along with broader population and economic development across the Mountain West-is driving substantial increases in electricity peak loads and utility customer counts, pointing toward robust, sustained volumetric growth and upward pressure on long-term revenue.

- Large-scale capital investments-such as the Ready Wyoming transmission expansion, Lange II natural gas generation, and Colorado Clean Energy Plan renewables projects-are expected to materially expand Black Hills' regulated rate base, enabling predictable, above-sector-average long-term earnings and net margins through constructive rate recovery mechanisms and innovative tariffs.

- Successful execution of regulatory strategies-including frequent, constructive rate reviews and timely rider mechanisms-has ensured rapid recovery of over $1.3B in recent system investments and will continue supporting cash flow stability and net margin expansion as capital projects ramp over the next several years.

- Tech-driven industrial load, specifically from major customers like Microsoft and Meta, is forecast to contribute over 10% of total EPS by 2028, and new load agreements (including those not yet in current five-year forecasts) offer upside, underpinning long-term EPS and revenue growth potential above current conservative financial guidance.

- The combination of grid modernization, enhanced resiliency initiatives, and the ability to attract tech customers in regulated territories positions Black Hills to benefit from sustainable financing advantages, potentially lowering capital costs and further improving capital efficiency and future earnings generation.

Black Hills Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Black Hills's revenue will grow by 16.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.6% today to 15.9% in 3 years time.

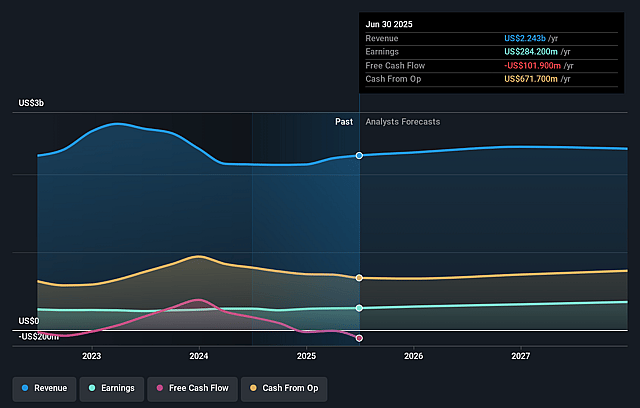

- Analysts expect earnings to reach $578.3 million (and earnings per share of $5.11) by about June 2029, up from $288.3 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $802.5 million in earnings, and the most bearish expecting $424.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.4x on those 2029 earnings, down from 19.7x today. This future PE is lower than the current PE for the US Integrated Utilities industry at 21.2x.

- Analysts expect the number of shares outstanding to grow by 4.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy capital expenditure requirements for infrastructure projects (e.g., Ready Wyoming transmission expansion, Lange II generation, Colorado Clean Energy Plan) create ongoing pressure on cash flows, and if regulatory recovery lags or costs overrun, this could compress net margins and limit earnings growth.

- Significant projected revenue growth relies on continued ramp-up of large, concentrated, and potentially volatile data center and blockchain load, exposing Black Hills to demand risk if these customers delay, cancel, or reduce commitments, directly impacting revenues and future earnings.

- The company's core dependence on regulated natural gas operations and geographic concentration in the Mountain West and Midwest makes Black Hills vulnerable to asset stranding, tightening emissions regulation, or region-specific economic/demographic stagnation, potentially affecting long-term revenue and net earnings.

- If distributed energy resources (DERs), renewables, and battery storage adoption accelerate more rapidly than Black Hills anticipates, traditional load growth could be undermined, eroding revenue streams and increasing the risk of under-recovery of fixed costs over the long-term.

- Rising frequency and severity of extreme weather events (e.g., wildfires), even with mitigation programs, may drive up insurance premiums, O&M expenses, and reliability investments, pressuring operating costs and potentially reducing net margins over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $83.4 for Black Hills based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.6 billion, earnings will come to $578.3 million, and it would be trading on a PE ratio of 15.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of $74.56, the analyst price target of $83.4 is 10.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Black Hills?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.