Last Update 16 Jul 26

Fair value Increased 15%JBHT: Tight Capacity And Intermodal Strength Will Support Shares With Balanced Risk

Analysts increased the JB Hunt Transport Services fair value estimate by about $37 to $288.18, citing higher price targets across the Street. These targets are supported by expectations for tighter truckload capacity, improving freight demand, and constructive intermodal and brokerage trends.

Analyst Commentary

Recent Street research on J.B. Hunt Transport Services highlights a mix of optimism about the freight cycle and intermodal growth, along with some caution around how much of that recovery is already reflected in the stock price. Price targets span a wide range, and ratings run from Underweight to Overweight. This provides a useful cross section of how different analysts are thinking about valuation, execution, and growth for J.B. Hunt.

Bullish Takeaways

- Bullish analysts see J.B. Hunt as well positioned to benefit from tighter truckload capacity and improving demand. They link this to higher contract pricing and a more supportive earnings backdrop into upcoming reporting periods.

- Several firms highlight intermodal as a key driver, citing expectations for modal conversion from truck to rail and share gain opportunities that could support revenue per load and margin resilience over time.

- Some bullish research points to structural capacity attrition in truckload, which is seen as pushing incremental freight onto rail and into J.B. Hunt’s network. This is viewed as supporting stronger bid season outcomes and, in their view, higher justified price targets.

- Positive views also focus on an early phase freight recovery, where an improving industrial backdrop, healthier import volumes, and disciplined industry capacity are expected to underpin better earnings momentum through 2027.

Bearish Takeaways

- Bearish analysts, including those at Morgan Stanley, acknowledge an improved outlook but argue that the freight cycle is already elevated. They see potential for volatility that could limit upside relative to current expectations.

- Some neutral or Hold ratings reflect concerns that recent price target revisions and a stronger freight setup may already be largely reflected in J.B. Hunt’s valuation, leaving a less compelling near term risk or reward profile.

- Several research notes stress that, while the medium term backdrop is constructive, near term results across transports may remain mixed. This could lead to choppier stock performance if execution or pricing trends fall short of current forecasts.

- There is also caution that, even with improving fundamentals, broader transport sector corrections remain a risk, which could weigh on J.B. Hunt’s shares regardless of company specific progress on intermodal or dedicated growth.

What’s in the News for J.B. Hunt Transport Services

- Several major firms, including Bernstein, Evercore ISI, Stephens, and Goldman Sachs, recently raised price targets on J.B. Hunt Transport Services, with ratings ranging from Neutral to Overweight and Outperform, citing a strong business model and an improving transportation sector outlook. Source: Multiple Upgrades Lift JB Hunt Transport Price Targets Amid Strong Sector Outlook.

- Bernstein upgraded J.B. Hunt to Outperform on July 10, 2026, lifting its price target from US$192 to US$329 and pointing to earnings potential and structural changes in the intermodal market as key supports. Source: Multiple Upgrades Lift JB Hunt Transport Price Targets Amid Strong Sector Outlook.

- J.B. Hunt reported Q1 2026 revenue growth of 5% and operating income growth of 16%, supported by record intermodal volume, higher productivity in Intermodal and Dedicated Contract Services, and an approximate 96% customer retention rate in dedicated services. Source: J.B. Hunt Reports Strong Q1 2026 Growth with Record Intermodal Volume and High Customer Retention.

- The company has been returning capital to shareholders through dividend increases, share repurchases, and a buyback program that has retired 967,677 shares for about US$210.06 million, and is also investing in artificial intelligence tools to improve efficiency and cost management. Sources: J.B. Hunt Reports Strong Q1 2026 Growth with Record Intermodal Volume and High Customer Retention, Buyback Tranche Update.

- J.B. Hunt is scheduled to report Q2 2026 earnings on July 15 after the close, with analysts projecting diluted EPS near US$1.70 and revenue around US$3.21b, and the stock has been added to the Russell 1000 Dynamic Index, drawing increased institutional interest while some analysts flag valuation concerns versus a consensus price target around US$251.45. Source: J.B. Hunt Prepares to Report Strong Q2 2026 Earnings with Upbeat Forecast and Russell 1000 Inclusion.

Valuation Changes for J.B. Hunt Transport Services

- Fair Value: Updated estimate has risen from $251.45 to $288.18, an increase of about 14.6%.

- Discount Rate: Assumed discount rate has edged down slightly from 8.17% to 8.15%.

- Revenue Growth: Modeled long term revenue growth rate has moved higher from 6.89% to 8.35%.

- Net Profit Margin: Assumed net profit margin has increased from 6.45% to 6.88%.

- Future P/E: Implied future P/E multiple has shifted up from 29.0x to 29.9x.

Key Takeaways

- Improved equipment utilization and cost optimization efforts enhance operational efficiencies, positively affecting net margins and profitability.

- Strategic investments in technology and capacity expansion support long-term revenue growth by accessing large addressable markets.

- Inflationary pressures, competitive rates, and muted demand in key segments challenge margins and earnings amidst an uncertain macroeconomic and policy environment.

Catalysts

About J.B. Hunt Transport Services- Provides surface transportation, delivery, and logistic services in the United States.

- Record first quarter intermodal volumes could indicate an ability to capture more market share, contributing to potential revenue growth.

- Efforts to improve equipment utilization and reduce empty move costs may enhance operational efficiencies, positively impacting net margins.

- Strategic investments in technology and capacity expansion may provide a platform for long-term revenue growth by better serving large addressable markets.

- Successful bid season outcomes, including modest rate increases and filling costly empty lanes, could drive better revenue and profitability metrics.

- The focus on reducing and optimizing costs, combined with a disciplined capital allocation strategy, suggests improvements in earnings as the company scales operations.

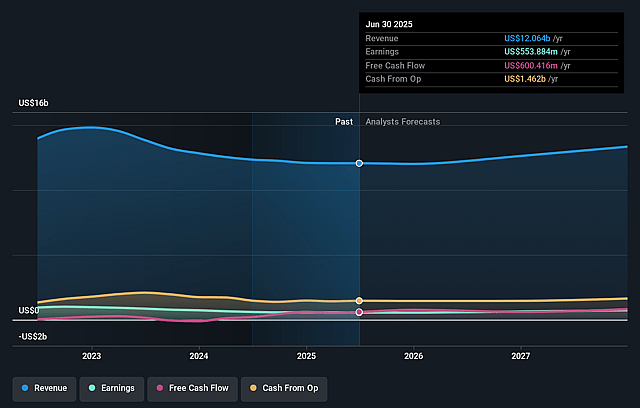

J.B. Hunt Transport Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming J.B. Hunt Transport Services's revenue will grow by 8.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.1% today to 6.9% in 3 years time.

- Analysts expect earnings to reach $1.1 billion (and earnings per share of $11.8) by about July 2029, up from $622.1 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $1.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.9x on those 2029 earnings, down from 41.9x today. This future PE is lower than the current PE for the US Transportation industry at 41.5x.

- Analysts expect the number of shares outstanding to decline by 2.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.15%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company faces a challenging operating environment with inflationary cost pressures more than offsetting productivity improvements, affecting margins and earnings.

- Lower yields and increased insurance premiums have been weighing on operating income, indicating potential pressure on net margins and earnings.

- Seasonally lower volume and rate pressure coupled with competitive truckload rates, especially in the Eastern network, may limit the ability to achieve desired price increases and hurt revenue and margins.

- Demand for Final Mile services such as furniture and appliances remains muted, potentially impacting revenue and margin growth in this segment.

- The uncertain macro environment and changing trade policies, including tariffs, pose risks to supply and demand dynamics, which could impact revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $288.18 for J.B. Hunt Transport Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $360.0, and the most bearish reporting a price target of just $171.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $15.4 billion, earnings will come to $1.1 billion, and it would be trading on a PE ratio of 29.9x, assuming you use a discount rate of 8.2%.

- Given the current share price of $276.28, the analyst price target of $288.18 is 4.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on J.B. Hunt Transport Services?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.