Last Update 15 Jul 26

Fair value Decreased 2.17%GGG: Cautious Downgrades Will Set Up Future Rebound Opportunity

Graco's updated analyst price target has edged down from $92 to $90. Analysts cite muted visibility on a return to growth and relatively more attractive opportunities in other industrial stocks as key reasons for the adjustment.

Analyst Commentary

Recent research on Graco highlights a mix of patience and caution as analysts reassess the stock's risk and reward trade off, largely around growth visibility and relative value versus other industrial peers.

Bullish Takeaways

- Some bullish analysts still see Graco as a quality industrial company, but view it as fairly valued rather than deeply discounted, which supports more neutral ratings such as Peer Perform.

- The shift to a neutral stance without a specific price target suggests these analysts are not calling for a major reset in valuation, but rather a pause while growth trends become clearer.

- Lagging performance versus certain peers over the last couple of years can be interpreted by bullish analysts as creating a potential setup for future catch up if execution and demand trends stabilize.

Bearish Takeaways

- Bearish analysts highlight that visibility into a return to growth is described as relatively muted, which tempers confidence in near term earnings momentum and can cap valuation upside.

- The downgrade to a peer level rating signals concern that Graco may not currently offer a compelling risk reward profile versus other industrial and electrical equipment stocks covered in the same sector.

- With other companies in the group viewed as offering potentially more attractive opportunities, some investors may see a higher opportunity cost in allocating fresh capital to Graco at current levels.

- The combination of limited growth visibility and competition for capital within the industrial sector keeps the stock more vulnerable to further cautious research updates if execution data points do not improve.

What’s in the News for Graco

- No recent Graco specific news items are available from the provided primary news sources.

- No Graco related coverage is available from the provided periodicals list.

- No recent Graco key developments are listed in the supplied sources.

Valuation Changes for Graco

- Fair Value: The assessed fair value has been adjusted slightly lower from $92 to $90.

- Discount Rate: The discount rate has edged down from 8.35% to 8.26%.

- Revenue Growth: The modeled revenue growth rate has moved marginally from 6.55% to 6.49%.

- Net Profit Margin: The projected net profit margin has shifted slightly from 23.99% to 23.95%.

- Future P/E: The future P/E multiple has been reduced modestly from 29.78x to 29.16x.

Key Takeaways

- New products and strategic U.S. manufacturing position Graco to increase market share and improve net margins amidst trade tensions.

- Integration of acquisitions and share repurchases aim to enhance revenue and shareholder value, supporting earnings growth.

- Tariff impacts, acquisition costs, and market dependencies pose risks to Graco's profitability and revenue growth amid uncertain trade policies and market conditions.

Catalysts

About Graco- Designs, manufactures, and markets systems and equipment used to move, measure, mix, control, dispense, and spray fluid and powder materials in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

- Graco is focused on increasing its market share by launching new products in the Contractor segment over the next few quarters, which is expected to drive revenue growth as new products gain traction.

- The strategic decision to maintain a strong U.S. manufacturing footprint may give Graco an advantage over competitors who manufacture offshore, especially in light of ongoing trade tensions and tariffs, potentially improving net margins due to cost control and pricing power.

- The company is expecting benefits from the integration of the COROB acquisition, aiming to capture more revenue and expand its presence in North America, which should contribute to earnings growth.

- Efforts to mitigate tariff impacts by qualifying additional suppliers and potentially redesigning products may stabilize or reduce cost of goods sold, supporting net margins over the coming quarters.

- Graco's active share repurchase program potentially boosts earnings per share, as evidenced by significant buybacks year-to-date, anticipating reduced share count and enhancing shareholder value.

Graco Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

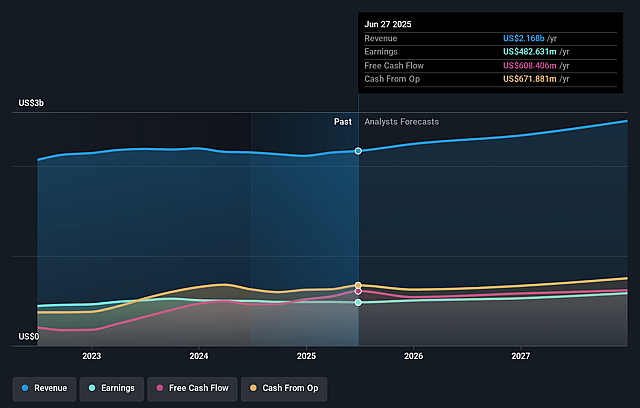

- Analysts are assuming Graco's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 23.0% today to 23.9% in 3 years time.

- Analysts expect earnings to reach $650.1 million (and earnings per share of $3.93) by about July 2029, up from $516.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.3x on those 2029 earnings, up from 23.7x today. This future PE is greater than the current PE for the US Machinery industry at 26.7x.

- Analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.26%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Tariffs and trade policies, especially those between the U.S. and China, pose a risk of decreasing revenues by 1% to 2%, as well as impacting the cost of goods sold due to potential tariffs on imports and retaliatory tariffs on exports.

- A combination of diminished gross margins due to higher product costs and lower factory volumes, along with the impact of acquisitions, could strain the net margins.

- Declining contractor segment operating margin rates, partly due to acquisitions and lower sales, might affect overall profitability.

- Dependence on inventory adjustments and strategic pricing actions to mitigate tariff impacts introduces uncertainty, which might lead to fluctuating earnings.

- Exposure to shaky professional paint and EMEA markets might limit growth opportunities and impact future revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $90.0 for Graco based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $100.0, and the most bearish reporting a price target of just $84.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.7 billion, earnings will come to $650.1 million, and it would be trading on a PE ratio of 29.3x, assuming you use a discount rate of 8.3%.

- Given the current share price of $73.81, the analyst price target of $90.0 is 18.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Graco?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.