Catalysts

About J.B. Hunt Transport Services

J.B. Hunt Transport Services provides transportation and logistics services across Intermodal, Dedicated, Truckload, brokerage and Final Mile offerings in North America.

What are the underlying business or industry changes driving this perspective?

- Heavy investment in Intermodal capacity and technology has been made during a soft freight period. If highway to rail conversion progresses more slowly than management expects, the company could be left with underutilized assets that pressure revenue growth and limit earnings contribution from these projects.

- Management is targeting US$100 million of structural cost savings and highlighting AI, automation and process changes. If rising inflation in wages, benefits, equipment and insurance absorbs most of these gains, longer term net margin improvement may be far smaller than the current run rate suggests.

- Rail consolidation and changing Class 1 network structures could reduce J.B. Hunt’s bargaining power over time. If service patterns or access terms become less favorable, Intermodal pricing or volume mix could shift in ways that cap revenue growth and compress operating income.

- Dedicated and brokerage wins rely on customers consolidating freight with fewer, financially strong carriers. If shippers revert to more fragmented sourcing once capacity tightness or regulatory pressure eases, J.B. Hunt may face tougher pricing and mix, weighing on revenue per load and segment margins.

- Large buybacks and continued capital deployment into fleet, containers and technology are funded by current cash generation. If freight demand and rate conditions stay muted for longer than expected, returns on this capital could fall, limiting earnings growth and raising questions over the sustainability of current deployment levels.

Assumptions

This narrative explores a more pessimistic perspective on J.B. Hunt Transport Services compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming J.B. Hunt Transport Services's revenue will grow by 4.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 4.8% today to 6.5% in 3 years time.

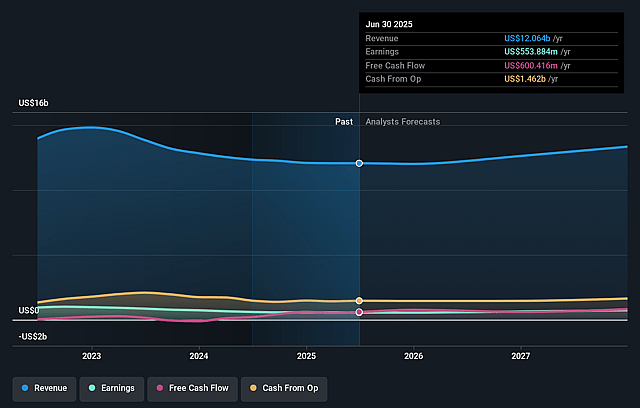

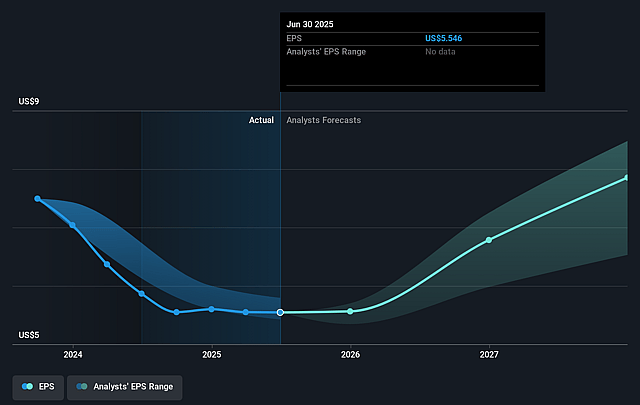

- The bearish analysts expect earnings to reach $905.0 million (and earnings per share of $9.87) by about January 2029, up from $572.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 17.2x on those 2029 earnings, down from 34.2x today. This future PE is lower than the current PE for the US Transportation industry at 32.4x.

- The bearish analysts expect the number of shares outstanding to decline by 4.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.09%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Management is heavily focused on operational excellence, with Intermodal and Highway services described as capturing additional volume and outperforming the market even while freight demand is soft. This focus could support steadier revenue and help protect earnings.

- The lowering cost to serve program has already removed more than US$20 million of structural costs in a single quarter toward a US$100 million target. Management links these efforts directly to better asset utilization and productivity, which could support higher net margins over time.

- The company reports that operating income improved 8% and diluted earnings per share improved 18% year over year on roughly flat revenue. This suggests that internal efficiency and cost controls are already having an effect on earnings despite muted demand.

- Customer feedback indicates shippers are consolidating freight with fewer, safe and financially solid carriers and are giving more business to providers like J.B. Hunt with strong service and diversified offerings. This trend could support long term volume, pricing power and revenue.

- Management highlights long term opportunities to convert highway shipments to Intermodal, growth in Eastern and Mexico related Intermodal volumes, and a healthy Dedicated sales pipeline with new truck deals and double digit margins. All of these factors could support revenue and earnings resilience over a multi year period.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for J.B. Hunt Transport Services is $150.0, which represents up to two standard deviations below the consensus price target of $178.04. This valuation is based on what can be assumed as the expectations of J.B. Hunt Transport Services's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $235.0, and the most bearish reporting a price target of just $150.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $13.9 billion, earnings will come to $905.0 million, and it would be trading on a PE ratio of 17.2x, assuming you use a discount rate of 8.1%.

- Given the current share price of $205.54, the analyst price target of $150.0 is 37.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on J.B. Hunt Transport Services?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.