Last Update07 May 25Fair value Decreased 1.00%

Key Takeaways

- Strategic repowering projects and a robust pipeline of gigawatt projects enhance growth prospects, positively impacting cash distribution and earnings.

- M&A activities and hedging strategies support financial stability, while self-funding growth initiatives bolster margins and future per-share cash distribution.

- Uncertain U.S. tariffs and permitting challenges, along with interest rate volatility and tax credit dependency, could elevate costs and hinder Clearway Energy's profitability and growth.

Catalysts

About Clearway Energy- Operates in the clean energy generation assets business in the United States.

- Clearway Energy is advancing on previously identified repowering opportunities, which include projects like Mt. Storm and San Juan Mesa. These initiatives are expected to extend the useful life of the assets, improve their risk profiles, and drive CAFD (Cash Available for Distribution) growth, impacting future EBITDA and CAFD positively.

- The company has a robust late-stage pipeline with over 9 gigawatts of projects, now reaching safe harbor investments for about 13 gigawatts, providing optionality and flexibility for future growth, potentially impacting revenues and earnings positively through increased capacity and new projects.

- Clearway is actively engaging in asset-centered third-party M&A, as demonstrated by the recent acquisitions of Tuolumne Wind and a solar project with long-term PPAs, promising additional CAFD yields of 10% to 13%. These acquisitions are expected to drive incremental CAFD per-share growth.

- Interest rate risks have been mitigated for the 2028 bond maturity through opportunistic hedging, improving financial stability and preserving net margins by controlling refinancing costs.

- The company anticipates generating significant retained CAFD from 2025 to 2027, contributing to self-funding growth. This approach is planned alongside prudent equity issuance, aiming to fund accretive growth investments and support the realization of the top end of the 2027 CAFD per-share growth targets, impacting overall earnings and net margins.

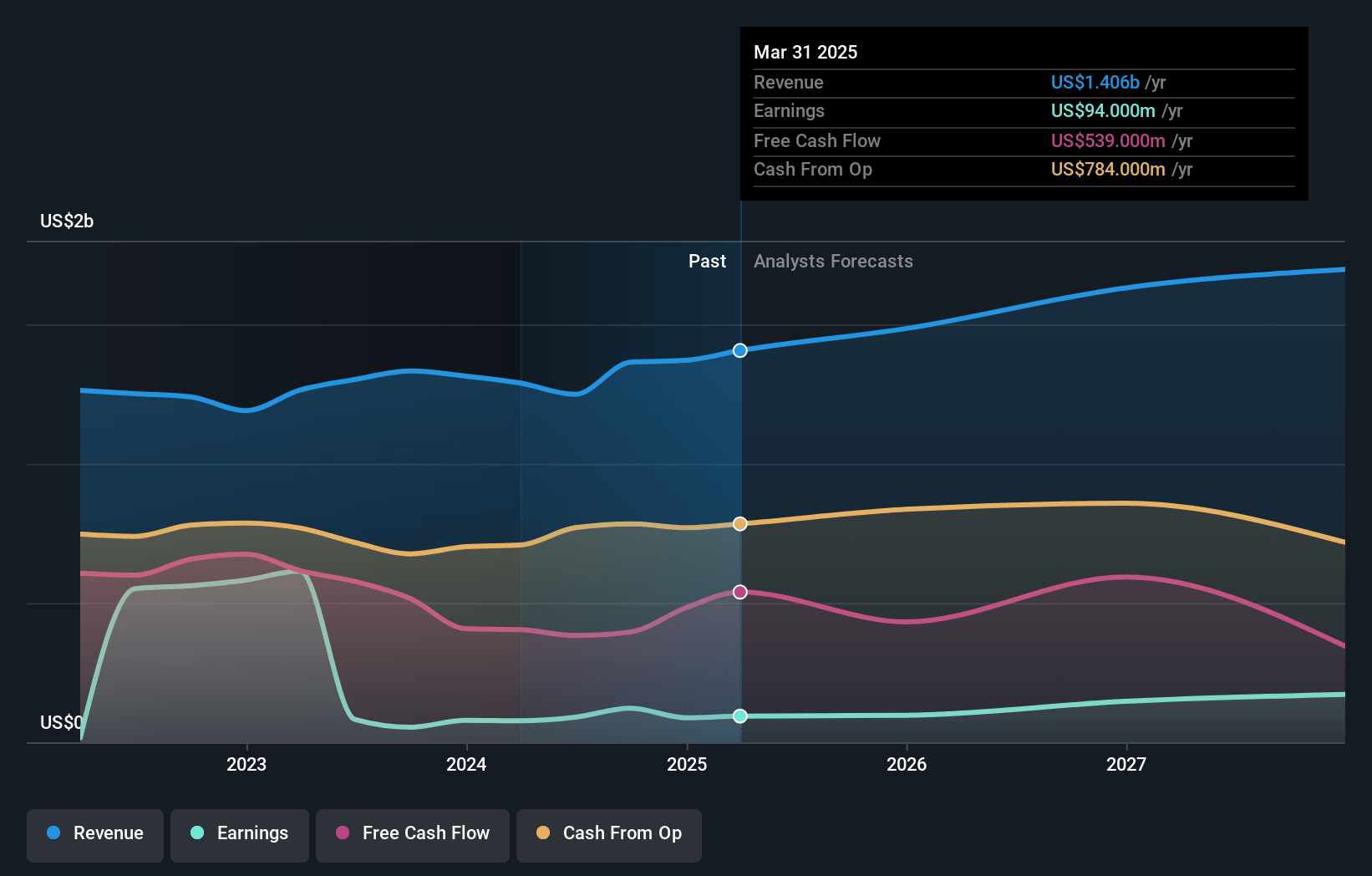

Clearway Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Clearway Energy's revenue will grow by 7.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.7% today to 9.9% in 3 years time.

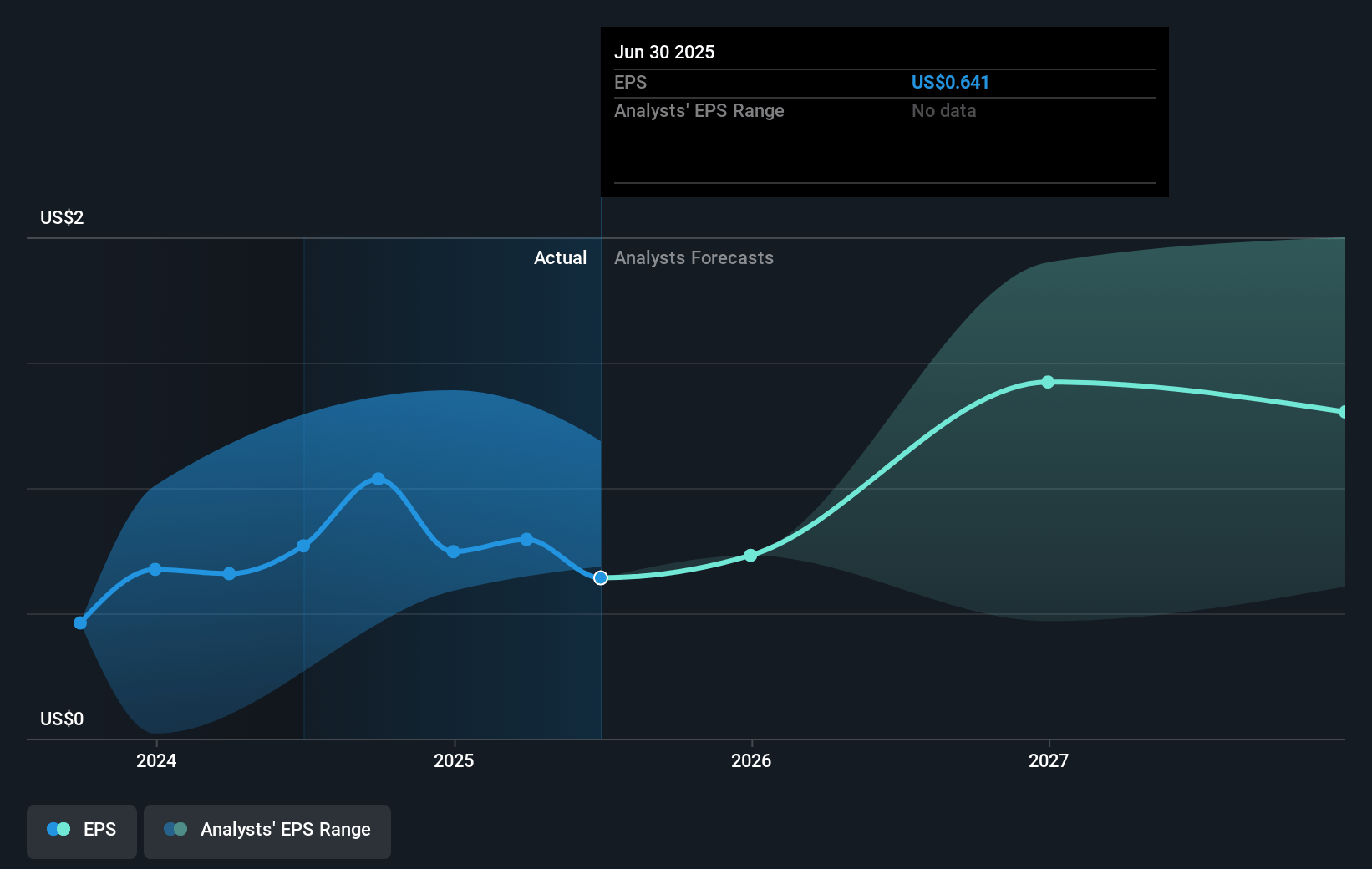

- Analysts expect earnings to reach $172.5 million (and earnings per share of $0.74) by about May 2028, up from $94.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $271.5 million in earnings, and the most bearish expecting $71.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 52.1x on those 2028 earnings, up from 33.8x today. This future PE is greater than the current PE for the US Renewable Energy industry at 25.6x.

- Analysts expect the number of shares outstanding to grow by 0.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.98%, as per the Simply Wall St company report.

Clearway Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Uncertainty around U.S. tariff policies, particularly those affecting battery imports from China, could lead to increased capital expenses for projects and impact overall profitability, potentially affecting future revenue and net margins.

- Challenges in the permitting process for wind repowering projects could lead to delays or additional costs, impacting the timeline for new revenue streams and cash flow generation.

- Dependency on traditional tax equity partnerships for monetizing tax credits may face changes or limitations, influencing financial structures and possibly reducing net earnings.

- Interest rate volatility poses a risk to refinancing plans for corporate bonds, potentially leading to higher interest expenses that could decrease net margins and limit funding for growth projects.

- The reliance on completing safe harbor investments to maintain a project pipeline through 2029 means any delays or disruptions could affect forecasted earnings and the ability to meet financial targets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $34.615 for Clearway Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.7 billion, earnings will come to $172.5 million, and it would be trading on a PE ratio of 52.1x, assuming you use a discount rate of 8.0%.

- Given the current share price of $26.92, the analyst price target of $34.61 is 22.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.