Narratives are currently in beta

Key Takeaways

- Anticipated significant rental growth and strategic capital investments position Prologis for enhanced revenue and long-term earnings improvement.

- Development in land banking and energy systems aims to support substantial future growth, cost savings, and improved net margins.

- Softening occupancy rates, rising bad debts, and slow development projects signal a challenging environment that may pressure Prologis's future revenues and margins.

Catalysts

About Prologis- Prologis, Inc. is the global leader in logistics real estate with a focus on high-barrier, high-growth markets.

- Prologis anticipates significant rental growth due to lease mark-to-market opportunities, with a potential net operating income (NOI) increase of $1.6 billion, impacting future revenue and earnings positively.

- The expansion of Prologis' land bank, including new development projects in India, positions the company for substantial future growth, which will likely enhance long-term revenue.

- The development of new energy systems, aiming for a generation capacity of 1 gigawatt by 2025, represents an opportunity for cost savings and additional revenue streams, potentially improving net margins.

- Strategic capital investments, including the acquisition of shares in Terrafina and expansion efforts in high-growth markets like Mexico, are likely to drive revenue growth and enhance strategic positioning.

- The current market rents being below replacement cost by approximately 15% suggest future potential rent increases, which could improve net effective rent change and support higher revenue and earnings over time.

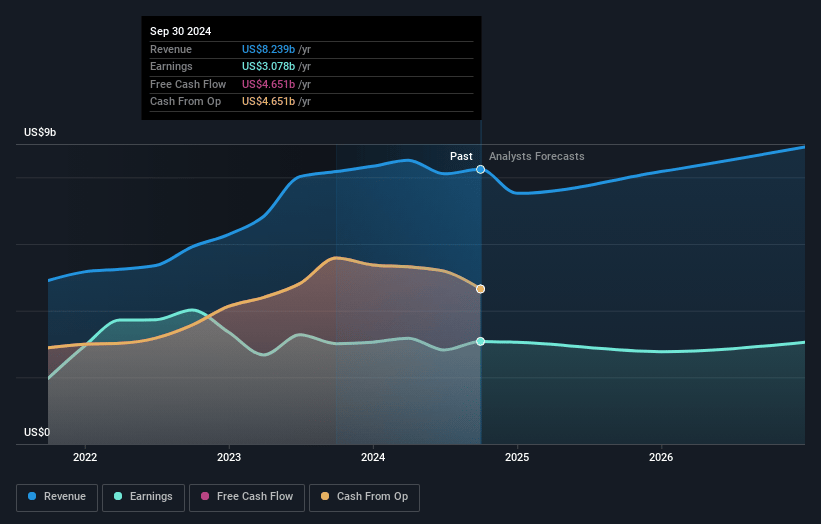

Prologis Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Prologis's revenue will grow by 5.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 37.4% today to 33.1% in 3 years time.

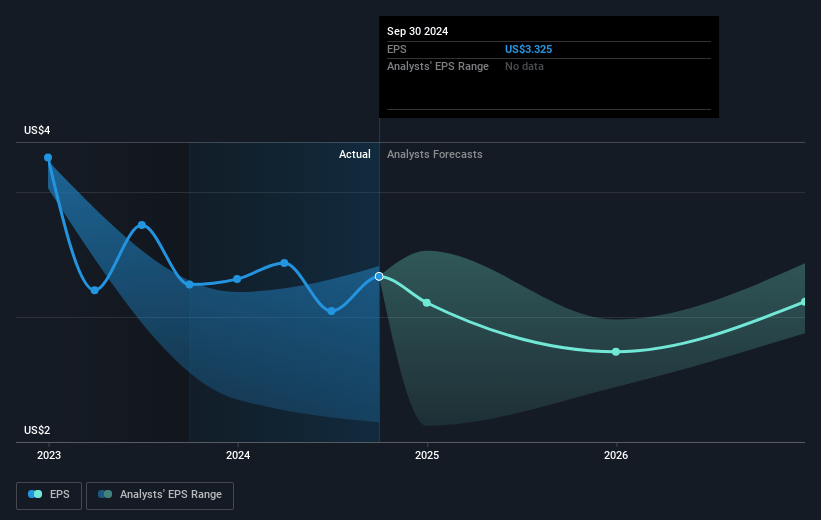

- Analysts expect earnings to reach $3.2 billion (and earnings per share of $3.41) by about November 2027, up from $3.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $3.9 billion in earnings, and the most bearish expecting $2.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 47.3x on those 2027 earnings, up from 35.0x today. This future PE is greater than the current PE for the US Industrial REITs industry at 36.0x.

- Analysts expect the number of shares outstanding to decline by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.89%, as per the Simply Wall St company report.

Prologis Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The softening of occupancy rates and rents, alongside subdued demand, indicates a challenging operating environment that could pressure revenues and net margins.

- The rise in bankruptcy filings contributing to elevated bad debt levels (from normal 15 to 20 basis points to 35 basis points) might negatively impact earnings and net margins.

- Market rents decreased approximately 3% globally this quarter, suggesting challenges in maintaining price levels which could strain future revenue growth.

- The slower decision-making in build-to-suit developments and the deferment of speculative development points to uncertainty in demand, potentially affecting future earnings growth.

- Increased levels of short-term leases raise uncertainties about tenant stickiness and could lead to volatility in future occupancy rates and rental revenues.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $132.25 for Prologis based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $154.0, and the most bearish reporting a price target of just $119.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $9.7 billion, earnings will come to $3.2 billion, and it would be trading on a PE ratio of 47.3x, assuming you use a discount rate of 6.9%.

- Given the current share price of $116.17, the analyst's price target of $132.25 is 12.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives