Last Update30 Jul 25Fair value Decreased 12%

Cantaloupe’s fair value estimate was reduced as its future P/E ratio rose sharply and net profit margin dropped considerably, suggesting declining earnings quality and higher valuation risk, resulting in the analyst price target falling from $12.70 to $11.20.

What's in the News

- Cantaloupe announced a definitive agreement to be acquired by 365 Retail Markets for approximately $830 million ($11.20 per share cash); the deal is unanimously approved by both boards and is subject to customary closing conditions.

- Leading up to the acquisition, Cantaloupe received multiple takeover bids exceeding $10 per share following a strategic review process.

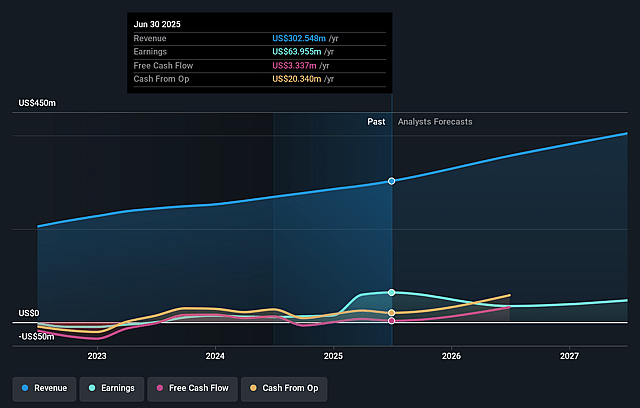

- The company revised fiscal year 2025 guidance, expecting total revenue between $302 million and $308 million, and net income between $64 million and $70 million.

- Cantaloupe formed a partnership with Carnival Cruise Line to provide POS technology for exclusive destination Celebration Key, extending Carnival’s cashless payment system to the island.

- Cantaloupe was dropped from multiple Russell value and small cap indexes, while being added to the Russell 2000 Defensive and Growth-Defensive indexes.

Valuation Changes

Summary of Valuation Changes for Cantaloupe

- The Consensus Analyst Price Target has significantly fallen from $12.70 to $11.20.

- The Future P/E for Cantaloupe has significantly risen from 20.38x to 31.54x.

- The Net Profit Margin for Cantaloupe has significantly fallen from 12.30% to 7.09%.

Key Takeaways

- Growth in micro markets and Smart Stores, along with international expansion, is driving revenue through higher transaction volumes and new market entry.

- Initiatives like micro-lending, digital advertising, and product innovations contribute to enhanced profitability and address capital, marketing, and operational challenges.

- High operating expenses from acquisitions and reliance on risky projections, micro markets, and domestic sales threaten growth amid market fluctuations and competition.

Catalysts

About Cantaloupe- A digital payments and software services company, provides technology solutions for self-service commerce market.

- Cantaloupe continues to see strong growth in micro markets and Smart Stores due to increased transaction volumes and customer expansion, which is likely to enhance revenue through greater penetration and higher sales per location.

- The company is expanding its international operations, particularly in Europe and Latin America, which is expected to drive future revenue growth as new markets are tapped and existing ones are expanded.

- The launch of the Cantaloupe Capital micro lending service aims to solve capital constraints for small and medium business customers, facilitating device and market expansion, potentially boosting equipment sales and subscription revenues.

- The Cantaloupe AdVantage program taps into digital advertising at point-of-sale devices, opening a new revenue stream that could improve net margins by leveraging existing assets for higher-margin advertising income.

- The integration of SB Software and new product innovations like Smart Store 600 and 700 are expected to drive revenue and profitability by addressing labor shortages and theft while capturing a wider range of retail opportunities.

Cantaloupe Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Cantaloupe's revenue will grow by 16.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.2% today to 12.3% in 3 years time.

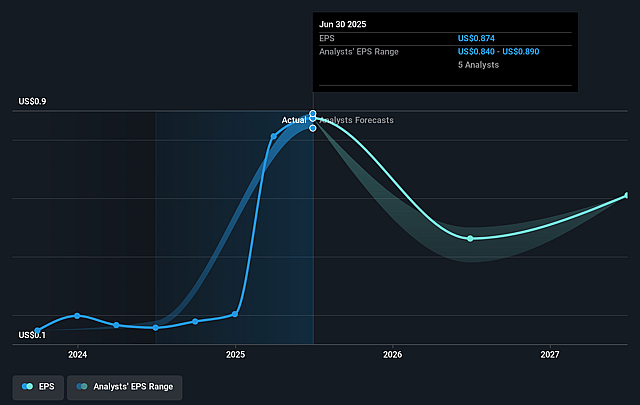

- Analysts expect earnings to reach $54.8 million (and earnings per share of $0.57) by about May 2028, up from $14.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.4x on those 2028 earnings, down from 39.8x today. This future PE is greater than the current PE for the US Diversified Financial industry at 14.2x.

- Analysts expect the number of shares outstanding to grow by 0.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.99%, as per the Simply Wall St company report.

Cantaloupe Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The financial results heavily rely on forward-looking statements, which are inherently risky as actual results may vary significantly from projections, affecting potential revenues and profits.

- The company incurs high operating expenses due to recent acquisitions, which can strain net margins and impact overall profitability if not managed efficiently.

- There is a significant dependency on micro markets and Smart Stores for growth, which could pose a risk if market demand fluctuates or competitors introduce similar products at more competitive rates, affecting future revenues.

- The international market contribution remains under 5% of total revenue, suggesting potential overreliance on the domestic market, which may hinder revenue growth during domestic economic downturns or market saturation.

- Equipment revenue has decreased by 7% compared to the prior year, which could indicate dwindling demand or increased competition in the equipment segment, posing a risk to overall revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $12.5 for Cantaloupe based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.0, and the most bearish reporting a price target of just $11.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $445.8 million, earnings will come to $54.8 million, and it would be trading on a PE ratio of 20.4x, assuming you use a discount rate of 7.0%.

- Given the current share price of $8.09, the analyst price target of $12.5 is 35.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.