Last Update 28 Nov 25

Fair value Decreased 3.04%PZZA: Ongoing Buyout Activity Will Drive Share Price Momentum Forward

Analysts have lowered their price target on Papa John's International from $49.30 to $47.80, citing declining growth and earnings outlooks. Recent buyout speculation has shifted the focus away from company fundamentals.

Analyst Commentary

Recent analyst discussions have highlighted the impact of ongoing buyout speculation on Papa John's International, underscoring both potential opportunities and notable concerns surrounding the company's valuation and future direction.

Bullish Takeaways

- There is renewed strategic interest in Papa John's. Multiple sources are reporting potential take-private bids, which may provide near-term support for the stock's valuation.

- The possibility of a takeover premium has kept investor focus high and has cushioned the share price despite operational uncertainty.

- Previous investments and engagement by significant firms have increased visibility and may result in a competitive bidding environment. This could be favorable for current shareholders.

- Analysts maintaining an optimistic outlook point to long-standing interest in strategic transactions as a signal that Papa John's remains an attractive asset within the sector.

Bearish Takeaways

- Bearish analysts are concerned that the ongoing buyout rumors have shifted attention away from core business fundamentals and performance metrics.

- The stock is considered to be trading in anticipation of a transaction rather than based on inherent growth prospects or earnings quality.

- Uncertainty regarding the realization of a formal bid and potential shifts in deal terms could introduce share price volatility and downside risk.

- Analysts warn that if buyout interest fails to materialize or sentiment around strategic alternatives fades, the valuation may correct to reflect Papa John's recent operational challenges.

What's in the News

- Hedge fund Irenic Capital acquired a stake in Papa John's in Q3, adding to speculation about the company's direction (Reuters).

- Reports surfaced that Papa John's is nearing a $65 per share take-private buyout by TriArtisan Capital. This news sparked a 9% jump in shares and a temporary trading halt (ABC Money).

- A person familiar with the situation denied the $65 per share buyout rumor. As a result, shares retracted from earlier highs but remained up about 10% (Seeking Alpha).

- Apollo Global withdrew its $64 per share bid to take Papa John's private, reportedly due to concerns about consumer spending and industry performance (Reuters).

- Rumors of additional suitors for Papa John's continue to circulate, highlighted by industry blogs and M&A-focused reporting (Betaville, The Fly).

Valuation Changes

- Consensus Analyst Price Target has fallen slightly from $49.30 to $47.80, reflecting reduced confidence in the company’s near-term outlook.

- Discount Rate has risen marginally from 10.01% to 10.10%, indicating a modest increase in perceived risk or required return by analysts.

- Revenue Growth projections have shifted from a positive 0.73% to a negative 0.82%, marking a significant downward revision and suggesting contraction expectations.

- Net Profit Margin estimates have decreased from 6.21% to 5.13%, highlighting weaker anticipated profitability.

- Future P/E Ratio has increased from 16.36x to 20.16x, suggesting reduced earnings expectations relative to the company's valuation.

Key Takeaways

- Strategic product innovation and enhanced menu offerings aim to boost revenue growth through increased customer engagement and sales.

- International expansion and cost efficiencies in restaurant operations are expected to drive revenue growth and improve net margins.

- Declines in sales and increased costs from strategic investments and marketing pressure margins, potentially hindering profit and cash flow growth.

Catalysts

About Papa John's International- Operates and franchises pizza delivery and carryout restaurants under the Papa Johns trademark in the United States, Canada, and internationally.

- Papa John's strategic focus on product innovation and enhancing the menu with new offerings is expected to boost revenue growth by increasing customer engagement and driving higher ticket sales.

- The investment of up to $25 million in marketing, including CRM capabilities and the Papa Rewards loyalty program, aims to drive greater customer loyalty and frequency, which should positively impact revenue.

- Efforts to reduce restaurant build costs and refranchise company-owned locations to growth-oriented franchisees are expected to improve net margins by enhancing operational efficiency and scale.

- The international expansion with emphasis on key growth markets, such as the Middle East and Latin America, aims to generate higher average unit volumes, contributing to revenue growth and increased earnings.

- The review of the North American commissary and distribution network to improve supply chain efficiency is likely to enhance franchisee profitability and support net margins through cost savings.

Papa John's International Future Earnings and Revenue Growth

Assumptions

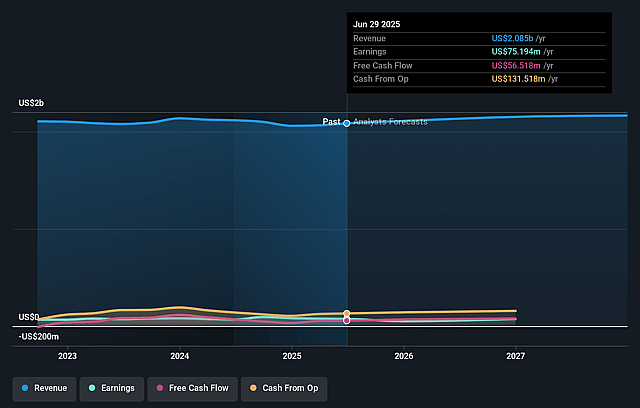

How have these above catalysts been quantified?- Analysts are assuming Papa John's International's revenue will grow by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 3.6% today to 3.1% in 3 years time.

- Analysts expect earnings to reach $67.4 million (and earnings per share of $2.0) by about September 2028, down from $74.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.1x on those 2028 earnings, up from 21.4x today. This future PE is greater than the current PE for the US Hospitality industry at 23.9x.

- Analysts expect the number of shares outstanding to grow by 0.36% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.14%, as per the Simply Wall St company report.

Papa John's International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The global system-wide restaurant sales declined by approximately 8% due to the additional week of operations in the prior year, indicating a lack of growth in actual sales, which can affect revenue and earnings.

- North America comparable sales were down 4% in the fourth quarter, impacted by strategic pricing decisions and a focus on value offerings, potentially affecting net margins negatively due to increased pressure on tickets.

- International comparable sales were cautiously projected to be flat to up 2% due to a dynamic operating environment, indicating potential risks in achieving meaningful growth, impacting overall revenue and earnings.

- The guidance for adjusted EBITDA projects a decrease from $227 million in 2024 to between $200 million and $220 million in 2025, due to continued strategic investments, which could strain profit margins and earnings.

- An increased marketing spend of up to $25 million and high commodity prices are expected to pressure operating margins, and if not offset by revenue growth, they could negatively impact net margins and cash flows.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $52.1 for Papa John's International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $67.0, and the most bearish reporting a price target of just $42.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.2 billion, earnings will come to $67.4 million, and it would be trading on a PE ratio of 34.1x, assuming you use a discount rate of 10.1%.

- Given the current share price of $48.76, the analyst price target of $52.1 is 6.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.