Last Update 11 Dec 25

SMBC: Future Returns Will Reflect Stable Earnings And Balanced Risk Reward Profile

Analysts have raised their price target on Southern Missouri Bancorp to $63 from $61, reflecting increased confidence in the bank's valuation while maintaining a neutral outlook.

Analyst Commentary

Bullish analysts view the higher price target as a sign that the bank's earnings power and return profile are better aligned with current market valuations than previously assumed.

They note that the new target implies incremental upside from current levels, but still reflects a balanced risk reward framework, consistent with a neutral rating on the shares.

Bullish Takeaways

- Bullish analysts highlight steady core profitability and credit quality trends that support a modestly higher valuation multiple.

- Improved visibility into loan growth and margin stability is seen as reducing downside risk to forward earnings estimates.

- Management's disciplined balance sheet strategy is viewed as enhancing capital flexibility and long term franchise value.

- The revised target suggests that execution on growth initiatives has been sufficiently strong to warrant a gradual re rating of the shares.

Bearish Takeaways

- Bearish analysts caution that the Market Perform stance signals limited near term upside despite the higher target.

- Concerns remain around the pace of loan growth in a slower economic backdrop, which could cap earnings acceleration.

- Net interest margin pressure and funding cost normalization are seen as potential headwinds to further valuation expansion.

- Competitive dynamics in Southern Missouri Bancorp's core markets may constrain fee income growth, keeping overall returns closer to sector averages.

What's in the News

- The board approves and implements Amended and Restated Bylaws, modernizing communication methods, adjusting the timing of the annual meeting, and clarifying leadership roles and authorities. (Key Developments)

- Bylaw changes explicitly permit director participation via video conference, broaden acceptable forms of electronic notice, and formalize the use of electronic and facsimile signatures for corporate actions. (Key Developments)

- The company reports net charge offs of 3.7 million for the quarter ended September 30, 2025, largely tied to a previously reserved 2.8 million special purpose CRE relationship. (Key Developments)

- The company completes the share repurchase program announced in May 2021, buying back a total of 239,835 shares, or 2.39 percent of shares outstanding, for 10.42 million. (Key Developments)

Valuation Changes

- Fair Value Estimate remains unchanged at approximately $63.50 per share, indicating no material revision to the intrinsic valuation.

- The discount rate has moved marginally from 6.96 percent to about 6.96 percent, reflecting a negligible change in the risk and return assumptions.

- Revenue growth is effectively unchanged at around 10.81 percent, suggesting stable expectations for top line expansion.

- Net profit margin remains steady at roughly 35.57 percent, indicating no meaningful shift in projected profitability.

- Future P/E is unchanged at about 8.97x, implying a consistent valuation multiple applied to forward earnings.

Key Takeaways

- Population shifts to core regions and technological investments are driving sustained growth in loans, deposits, efficiency, and customer relationships.

- Lower funding costs, strong loan pipelines, and disciplined credit strategies are expanding margins and supporting profitability despite sector-specific risks.

- Rising credit and asset quality risks, margin pressure, and industry consolidation threaten profitability and growth, while operational efficiency depends on successful technology investments.

Catalysts

About Southern Missouri Bancorp- Operates as the bank holding company for Southern Bank that provides banking and financial services to individuals and corporate customers in the United States.

- Migration of Americans to suburban and rural areas of the Midwest/South is increasing demand for community banking and lending services in Southern Missouri Bancorp's core regions, supporting sustained loan and deposit growth-positively impacting revenue and overall earnings.

- Enhanced adoption of digital banking among older/rural customers, supported by ongoing investments in technology and platform upgrades, is improving efficiency and deepening customer relationships, creating opportunities for cost reductions and higher net margins.

- Recent and expected future easing of deposit competition allows the bank to lower funding costs, as seen with reduced CD rates and a stable deposit base, leading to potential net interest margin expansion and improved profitability through fiscal 2026.

- Strong loan origination pipeline, with new loans being booked at higher yields than the existing portfolio, alongside the ability to reprice loan assets upward as they mature, is supporting further net interest income and net margin growth.

- The company's disciplined approach to credit, proactive reserving for ag exposure, and readiness to leverage federal support programs in agriculture mitigates risk from temporary sector headwinds, supporting long-term asset quality and earnings resilience.

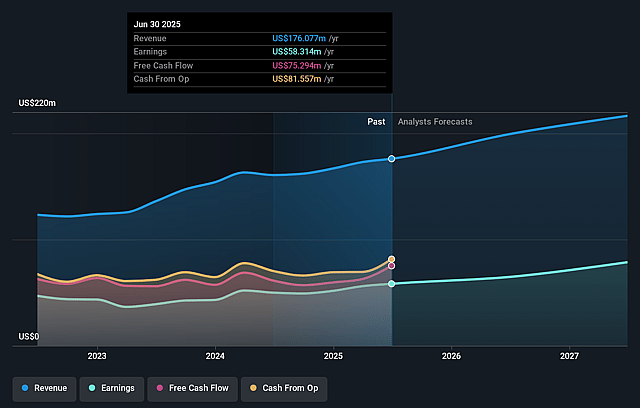

Southern Missouri Bancorp Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Southern Missouri Bancorp's revenue will grow by 10.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 32.4% today to 36.8% in 3 years time.

- Analysts expect earnings to reach $85.9 million (and earnings per share of $7.54) by about September 2028, up from $56.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.4x on those 2028 earnings, down from 11.3x today. This future PE is lower than the current PE for the US Banks industry at 11.9x.

- Analysts expect the number of shares outstanding to grow by 0.2% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.78%, as per the Simply Wall St company report.

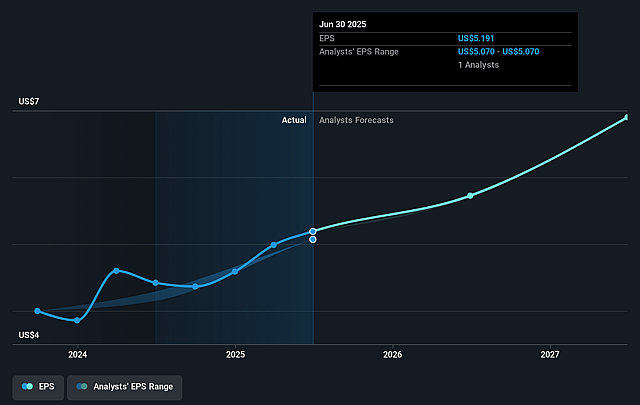

Southern Missouri Bancorp Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Deteriorating credit quality and increasing levels of nonperforming loans (NPLs)-notably within special purpose CRE and agricultural portfolios-pose a risk of further write-downs and loan loss provisions, which could pressure future earnings and profitability.

- The agricultural loan segment faces significant stress due to persistently low commodity prices, rising input costs, and weaker collateral coverage, raising the risk of higher delinquencies and asset quality deterioration, negatively impacting earnings and capital reserves.

- Ongoing margin expansion is partly dependent on continued loan growth and repricing, but anticipated higher prepayment activity (especially in nonowner-occupied CRE) could slow net loan growth, potentially limiting revenue and net interest income growth in the near-to-medium term.

- Increased reliance on technology investments and third-party data processing expenses, if not properly managed or if expected efficiencies fail to materialize, could elevate cost-to-income ratios and weigh on net margins over time.

- Industry consolidation pressures remain elevated, and Southern Missouri Bancorp may be compelled to pursue potentially dilutive M&A, or risk falling behind larger competitors, which could impact scale advantages, revenue growth, and long-term margin sustainability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $67.0 for Southern Missouri Bancorp based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $233.5 million, earnings will come to $85.9 million, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 6.8%.

- Given the current share price of $56.24, the analyst price target of $67.0 is 16.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Southern Missouri Bancorp?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.