Key Takeaways

- Aggressive investment in new markets, products, and digital infrastructure positions Ajanta for sustained above-industry growth and improved profitability across Asia and Africa.

- First-mover advantage in chronic and specialty therapeutics, coupled with rising global demand for generics, underpins margin expansion and robust long-term cash flow.

- Heavy reliance on traditional products, regulatory and supply chain risks, and a narrow therapeutic focus threaten earnings stability and growth amid industry changes.

Catalysts

About Ajanta Pharma- A pharmaceutical formulation company that develops, manufactures, and markets specialty pharmaceutical finished dosages.

- Analyst consensus anticipates Ajanta's Asian branded generics expansion to drive sustained growth, but this may be understated as Ajanta is aggressively investing in new launches, field force, and untapped therapeutic areas across underpenetrated Asian markets, positioning for above-consensus acceleration in revenue over the next three years as adoption of chronic therapies increases.

- While analysts broadly expect significant long-term gains from Ajanta's chronic therapies rollout and new product launches in Africa, they may underestimate the compounding impact of first-mover advantage in underpenetrated chronic disease segments and the company's ability to leverage rising healthcare investment across the continent, resulting in sustained double-digit sales growth and potential margin expansion as product mix shifts toward higher-value offerings.

- Ajanta is well-placed to outpace industry growth in high-margin specialty therapeutics such as dermatology, cardiology, and ophthalmology internationally, with increased prescription volumes driven by aging populations and the rising burden of chronic diseases, which is expected to boost both average selling prices and net margins.

- Superior operational execution and investments in robust digital supply chain infrastructure enable Ajanta to capitalize on global digitalization and telehealth trends, expanding its reach to new patient demographics and ensuring reliable product availability-supporting above-industry earnings growth and improved working capital turns.

- Building on its strong R&D commitment and the new liquid plant for emerging markets, Ajanta is positioned to exploit the global shift toward affordable generics and capitalize on accelerated genericization from patent expiries, driving a rapid and sustainable increase in both revenue and long-term cash generation.

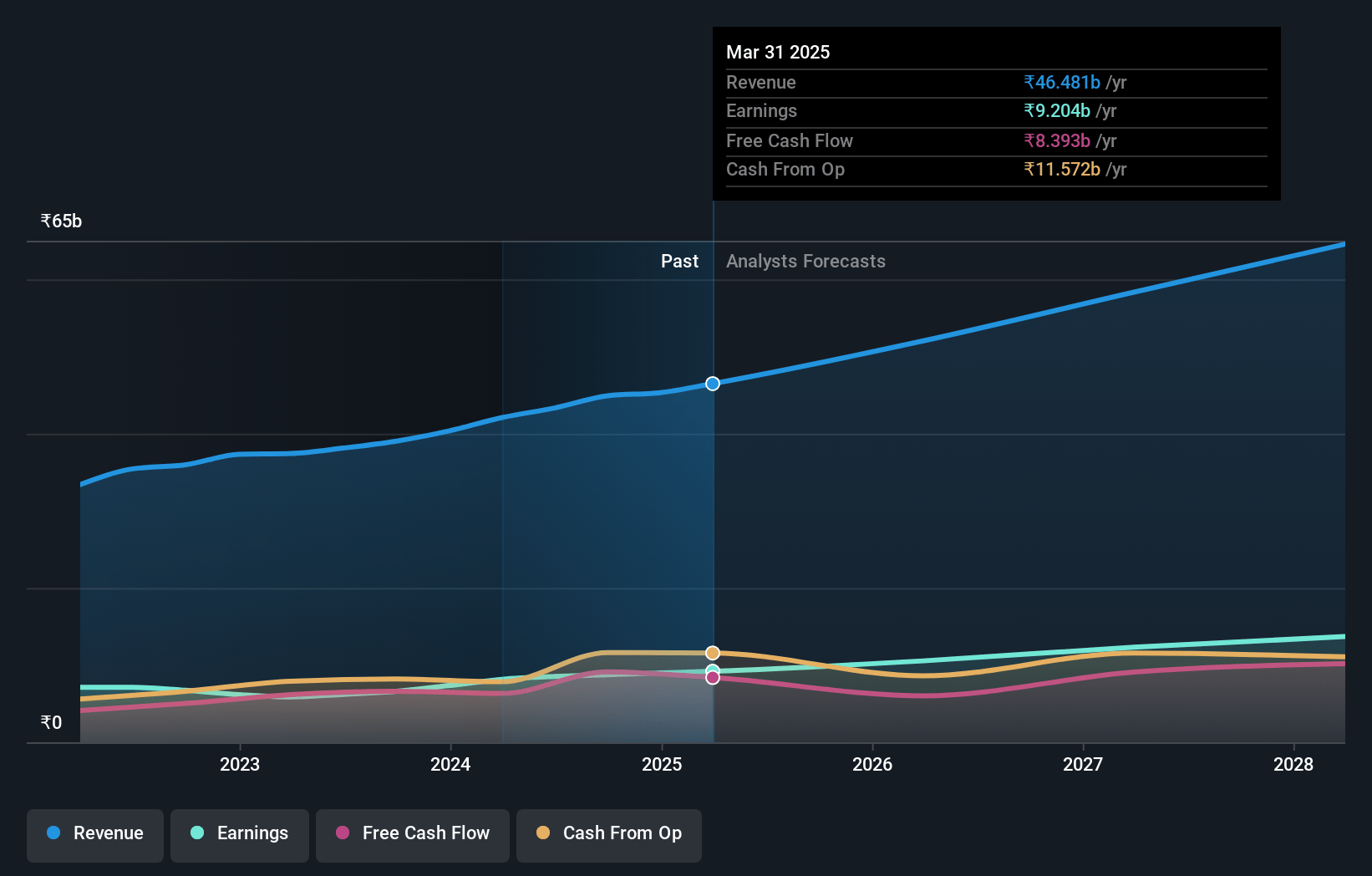

Ajanta Pharma Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Ajanta Pharma compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Ajanta Pharma's revenue will grow by 13.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 19.8% today to 22.0% in 3 years time.

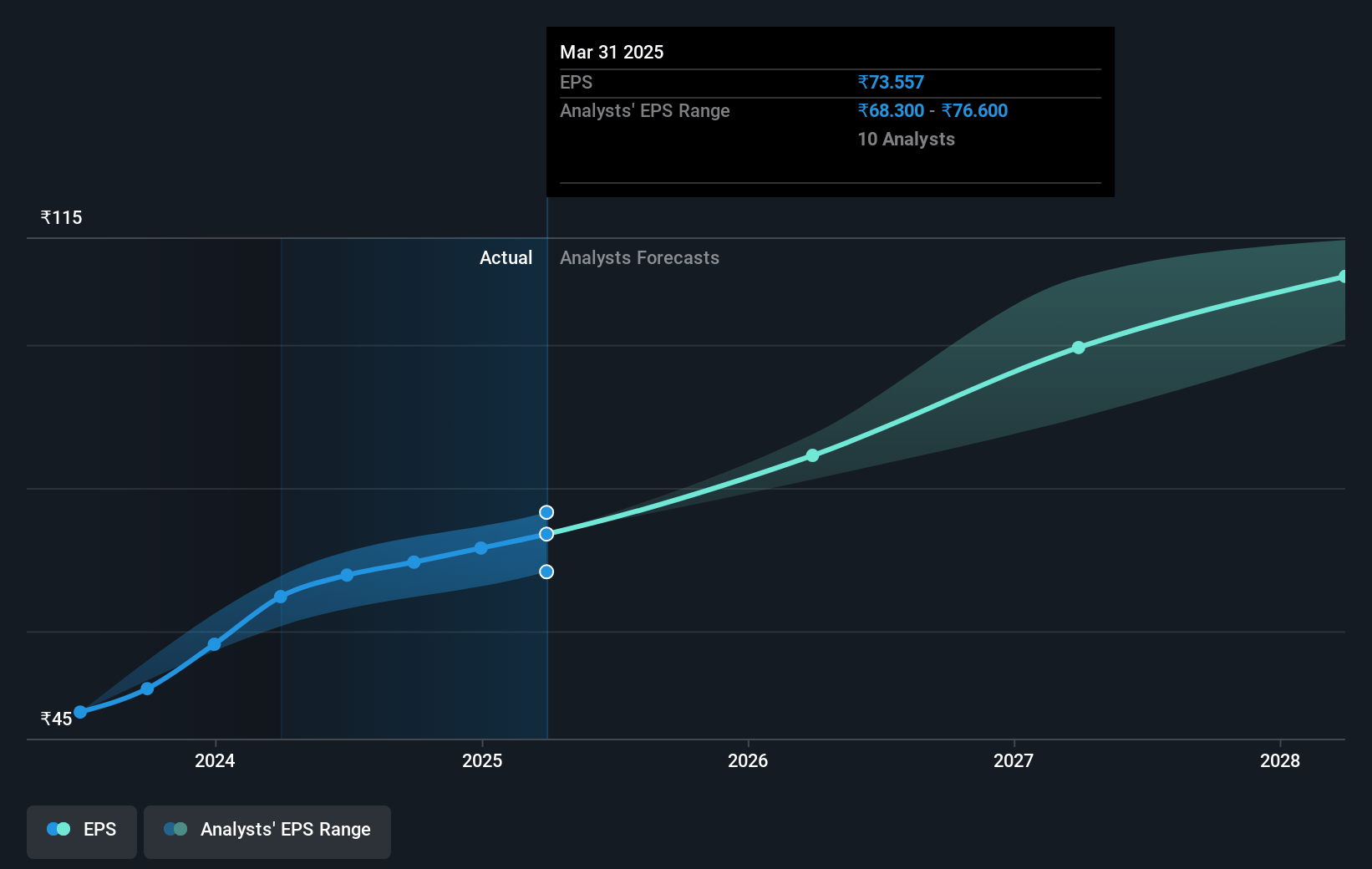

- The bullish analysts expect earnings to reach ₹14.8 billion (and earnings per share of ₹118.31) by about July 2028, up from ₹9.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 39.4x on those 2028 earnings, up from 35.6x today. This future PE is greater than the current PE for the IN Pharmaceuticals industry at 32.9x.

- Analysts expect the number of shares outstanding to decline by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.55%, as per the Simply Wall St company report.

Ajanta Pharma Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ajanta Pharma's heavy reliance on traditional branded generics exposes it to long-term risks from the industry shift toward biologics and personalized medicine, which may significantly dampen revenue growth and reduce future earnings.

- Increasing global regulatory scrutiny and healthcare cost containment trends are likely to result in higher compliance costs and intense pricing pressure, directly impacting Ajanta Pharma's margins and possibly slowing net profit growth.

- The company's portfolio remains highly concentrated in a few therapeutic areas such as ophthalmology and dermatology, making revenue growth vulnerable to demand shocks or heightened competition within these segments, potentially creating revenue volatility.

- Delays in ANDA filings, the slower pace of complex generic development, and setbacks in R&D (with some studies not being successful this year) may hinder Ajanta Pharma's ability to effectively replenish its pipeline, putting future earnings momentum at risk as older products lose exclusivity.

- Ajanta Pharma remains exposed to procurement and raw material risks due to dependence on imports from China, making its supply chain susceptible to geopolitical disruptions and rising input costs, which could compress net profit margins over the medium to long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Ajanta Pharma is ₹3293.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Ajanta Pharma's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3293.0, and the most bearish reporting a price target of just ₹1853.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be ₹67.0 billion, earnings will come to ₹14.8 billion, and it would be trading on a PE ratio of 39.4x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹2626.5, the bullish analyst price target of ₹3293.0 is 20.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.