Last Update 14 Dec 25

ARX: Dividend Hike And Buybacks Will Drive Stronger Future Shareholder Returns

Analysts have trimmed their price targets on ARC Resources, with recent revisions including cuts from C$35 to C$33 and from C$32 to C$30. They cited modestly softer growth assumptions, which are partly offset by slightly stronger margin expectations.

Analyst Commentary

Analyst sentiment around ARC Resources remains constructive overall, even as recent target price cuts reflect a more measured outlook on growth and capital efficiency. The stock is still broadly viewed as a quality upstream name, but expectations have been recalibrated to account for a more normalized commodity backdrop and disciplined spending plans.

Bullish Takeaways

- Bullish analysts continue to see upside to intrinsic value, as evidenced by target prices that remain well above the current trading range despite recent downward revisions.

- ARC Resources being added to key preferred lists signals confidence in the company’s ability to execute on its development plan and deliver competitive returns on capital over the medium term.

- Improved margin assumptions support the view that operating efficiency gains and a high quality asset base can sustain robust free cash flow even under more conservative growth forecasts.

- Balance sheet strength and disciplined capital allocation are cited as supports for ongoing shareholder returns, helping to underpin valuation multiples versus peers.

Bearish Takeaways

- Bearish analysts highlight that trimmed price targets reflect reduced growth expectations, suggesting less room for multiple expansion if production and cash flow growth slow further.

- Removal from some favored lists underscores concern that relative outperformance may narrow, particularly if peers with higher growth trajectories regain market attention.

- More cautious volume and pricing assumptions raise the risk that consensus estimates could still prove optimistic if commodity prices remain range bound.

- With valuation now closer to long term historical averages, some see limited near term re rating potential absent a clear catalyst or above plan execution on cost and productivity.

What's in the News

- The board has approved an 11% increase to the quarterly dividend, raising it from $0.19 to $0.21 per share (annually from $0.76 to $0.84 per share). This reinforces a growing shareholder returns framework tied to profitability and share count reduction (Key Developments).

- ARC has issued 2026 production guidance, targeting crude oil and condensate of 105,000 to 115,000 bbl/day, natural gas of 1,500 to 1,520 MMcf/day, and NGLs of 48,000 to 52,000 bbl/day, signaling confidence in its medium term growth profile (Key Developments).

- Third quarter 2025 results show total production rising to 359,236 boe/day from 326,768 boe/day a year earlier, with notable growth in crude oil, condensate, and NGL volumes, while natural gas volumes were modestly lower (Key Developments).

- Under the buyback launched in September 2024, ARC has repurchased 16,800,000 shares for CAD 444.2 million, representing 2.87% of shares outstanding, highlighting active capital returns beyond the dividend (Key Developments).

- ARC Resources has been added to the FTSE All World Index, potentially broadening its global investor base and passive fund ownership (Key Developments).

Valuation Changes

- Fair Value: Unchanged at approximately CA$30.94 per share, indicating a stable intrinsic value assessment despite other model adjustments.

- Discount Rate: Edged down slightly from 6.12% to 6.118%, implying a marginally lower required return and modestly supportive impact on valuation.

- Revenue Growth: Reduced slightly from about 4.20% to 4.17% annually, reflecting a more conservative top line growth outlook.

- Net Profit Margin: Increased modestly from roughly 24.14% to 24.58%, signaling improved profitability expectations that partially offset softer growth assumptions.

- Future P/E: Eased from 12.37x to 12.16x, suggesting a marginally lower implied valuation multiple on forecast earnings.

Key Takeaways

- Strategic asset integration, infrastructure investments, and operational efficiencies enhance production, profitability, and revenue resilience across commodity cycles.

- Focused capital discipline and shifting production mix drive higher margins, improved cash flow, and increased shareholder returns.

- Heavy dependence on Western Canadian gas, rising costs, expansion risks, and high shareholder payouts may threaten long-term financial stability amid market and regulatory uncertainty.

Catalysts

About ARC Resources- Engages in the acquiring and developing crude oil, natural gas, condensate, and natural gas liquids in Canada.

- Integration of recently acquired Kakwa assets and new Attachie acreage extends ARC's inventory life and enhances production scalability, supporting long-term growth in operating cash flow, revenue visibility, and net margin expansion as operational synergies and capital efficiencies are realized.

- The ramp-up of LNG Canada and growing LNG export capacity out of Western Canada is expected to increase regional natural gas demand and support stronger local pricing, directly benefiting ARC's realized revenue and improving the profitability of its large Montney natural gas resource base.

- Continued shift toward a higher liquids (condensate and light oil) production mix, combined with success in well design optimization (higher-intensity completions, wider spacing), is driving higher-margin output and improved capital efficiency, leading to higher EBITDA margins and free cash flow generation.

- ARC's disciplined approach to capital allocation-returning nearly 100% of free cash flow via dividends and buybacks, while maintaining a strong balance sheet-positions the company to drive sustained growth in free cash flow per share and total shareholder return.

- Early investments in pipeline and transportation infrastructure, along with long-term marketing contracts accessing premium-priced North American and international markets, enable ARC to outperform local price benchmarks and support stronger, more resilient revenues through commodity cycles.

ARC Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ARC Resources's revenue will grow by 6.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 26.4% today to 29.0% in 3 years time.

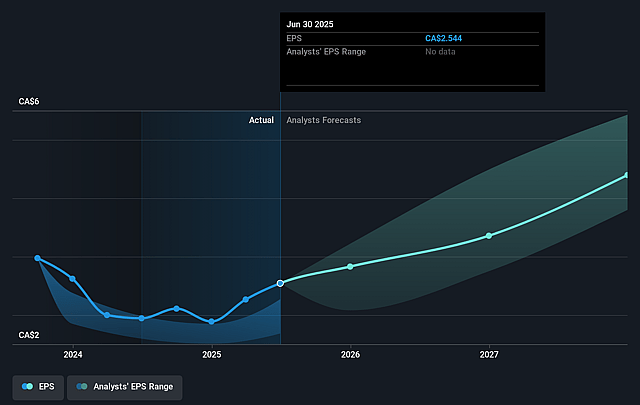

- Analysts expect earnings to reach CA$2.0 billion (and earnings per share of CA$3.93) by about September 2028, up from CA$1.5 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CA$1.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.2x on those 2028 earnings, up from 10.1x today. This future PE is lower than the current PE for the CA Oil and Gas industry at 12.2x.

- Analysts expect the number of shares outstanding to decline by 1.55% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.18%, as per the Simply Wall St company report.

ARC Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Heavy long-term reliance on natural gas and liquids in Western Canada leaves ARC vulnerable to structural declines in fossil fuel demand driven by global decarbonization and electrification, which could negatively impact revenue and market valuation over time.

- Rising operating costs from water handling, higher expense per BOE due to Sunrise shut-ins, and potential ongoing structural cost increases at Kakwa may compress net margins and erode profitability as commodity prices fluctuate.

- Substantial CapEx commitments for expansion projects (especially Attachie Phase 2 and Kakwa integration) expose ARC to cost overruns or lower-than-expected production returns, straining free cash flow and increasing financial risk if commodity prices are weak.

- Shut-ins of low-cost dry gas assets (like Sunrise) due to unfavourable pricing highlight the company's sensitivity to local oversupply, pipeline bottlenecks, and the risk that anticipated LNG demand may materialize more slowly than expected-undermining revenue and earnings.

- Increased leverage from recent debt-funded acquisitions, alongside a corporate policy of returning essentially all free cash flow to shareholders, may limit balance sheet flexibility and the ability to address ESG-driven capital allocation pressures or future regulatory costs, which could impact long-term earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$33.941 for ARC Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$38.0, and the most bearish reporting a price target of just CA$31.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$6.9 billion, earnings will come to CA$2.0 billion, and it would be trading on a PE ratio of 11.2x, assuming you use a discount rate of 6.2%.

- Given the current share price of CA$26.13, the analyst price target of CA$33.94 is 23.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ARC Resources?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.